Derivative Valuation, Risk Management, Volatility Trading

|

Are you looking for a way to save money on your mortgage and help the environment at the same time? If so, you may want to consider an energy efficient mortgage. An energy efficient mortgage is a type of home loan that allows you to finance energy-saving upgrades to your home. This can include things like installing new windows or insulation or upgrading your heating and cooling system. By making these upgrades, you can reduce your monthly energy bills, which will save you money over the life of your mortgage. What is an Energy Efficient Mortgage?An Energy Efficient Mortgage (EEM) is a type of mortgage that rewards borrowers for making energy efficient improvements to their homes. These improvements can range from installing solar panels to upgrading your insulation. Not only will you save money on your energy bill, but you'll also be doing your part to help the environment. How to apply for an Energy Efficient Mortgage?If you’re interested in an energy efficient mortgage, there are a few things you need to know. First, you’ll need to find a lender that offers this type of loan. Not all lenders do, so it may take some shopping around. Once you’ve found a lender, you’ll need to get a home energy assessment. This assesses your home’s energy efficiency and recommends improvements that will make your home more energy efficient. Once you’ve made the recommended improvements, you can then apply for an Energy Efficient Mortgage. The process is similar to applying for a regular mortgage, but you’ll need to provide documentation of the energy efficient improvements you’ve made to your home. What are the benefits of an Energy Efficient Mortgage?There are many benefits to an Energy Efficient Mortgage. Perhaps the most obvious benefit is that you’ll save money on your energy bill. But you’ll also be doing your part to help the environment by reducing your carbon footprint. And, if you ever decide to sell your home, these improvements can make your home more marketable. What are the drawbacks of an Energy Efficient Mortgage?There are a few drawbacks to consider before applying for an Energy Efficient Mortgage. First, you may need to put more money down upfront for the energy efficient improvements. Additionally, your monthly mortgage payments may be slightly higher than a regular mortgage. However, these drawbacks are typically offset by the money you’ll save on your energy bill. FAQsWhat is energy efficiency financing?Energy efficiency financing is a type of loan that helps you finance energy efficient improvements to your home. These loans are typically offered at a lower interest rate than a regular mortgage or home equity loan. What is the difference between an energy efficient mortgage and a regular mortgage?An energy efficient mortgage is a type of mortgage that rewards borrowers for making energy efficient improvements to their homes. A regular mortgage does not offer this incentive. How do I qualify for an energy efficient mortgage?To qualify for an energy efficient mortgage, you’ll need to find a lender that offers this type of loan and get a home energy assessment. Once you’ve made the recommended improvements, you can then apply for an Energy Efficient Mortgage. What is a sustainability mortgage?A sustainability mortgage is a type of loan that helps you finance sustainable improvements to your home. These loans are typically offered at a lower interest rate than a regular mortgage or home equity loan. What is the difference between an energy efficient mortgage and a sustainability mortgage?An energy efficient mortgage is a type of mortgage that helps you finance energy efficient improvements to your home. A sustainability mortgage helps you finance sustainable improvements to your home. The two are similar, but sustainability mortgages tend to have a broader definition of what counts as a sustainable improvement. What are energy loans?Energy loans are loans that help you finance energy efficient improvements to your home. These loans are typically offered at a lower interest rate than a regular mortgage or home equity loan. What is the difference between an energy efficient mortgage and an energy loan?An energy efficient mortgage is a type of mortgage that helps you finance energy efficient improvements to your home. An energy loan is a type of loan that helps you finance energy efficient improvements to your home. The two are similar, but energy loans tend to have a broader definition of what counts as an energy efficient improvement. Do I need to own my home to get an energy efficient mortgage?No, you do not need to own your home to get an Energy Efficient Mortgage. You can get an Energy Efficient Mortgage for a home that you are buying, building, or refinancing. How do I find a lender for an energy efficient mortgage?To find a list of lenders that offer Energy Efficient Mortgages, you can check out the Database of State Incentives for Renewables and Efficiency. How do I get a home energy assessment?A home energy assessment is an evaluation of your home’s energy efficiency. To get a home energy assessment, you can contact your local utility company or a certified home energy auditor. The bottom lineEnergy efficient mortgages are a great way to finance energy efficient improvements to your home. These loans offer a number of benefits, including lower interest rates and the potential to save money on your energy bill. If you’re thinking about making energy efficient improvements to your home, an energy efficient mortgage may be a good option for you. If you’re looking for a way to save money and help the environment, an energy efficient mortgage may be right for you. Talk to a lender today to see if you qualify. Originally Published Here: Energy Efficient Mortgages: How to Save Money and Help the Environment

0 Comments

A balance sheet is a financial statement that includes account balances from accounting systems. It classifies those balances under three categories, assets, liabilities, and equity. Primarily, it follows the accounting equation. This equation states the total of assets should equal the total of liabilities and equity. Therefore, the balance sheet presents those balances to show the requirement of the equation has been met. Most companies use a straightforward format for the balance sheet, which comes from accounting standards. However, some investors prefer other presentations, such as the classified balance sheet. What is a Classified Balance Sheet?A classified balance sheet follows the same format as a typical balance sheet. However, it rearranges some items to make them more readable. The classified balance includes assets, liabilities, and shareholders’ equity. It classifies these into subcategories of accounts. However, there is no standard method of preparing the classified balance sheet. Companies must choose how to present it. The classified balance sheet aggregates balances into several categories. While these categories depend on the company management's judgment, the goal is to make them more readable and accessible. Due to this approach, users can comprehend and extract information more easily. Primarily, the classified balance sheet provides organized details of the company's operations compared to the typical balance sheet. What is the format of the Classified Balance Sheet?The typical balance sheet comes with a standardized format from various accounting principles and standards. However, the classified one does not have these requirements. Usually, companies include several subheadings in the classified format to expand and categorize information better. Some of the categories within the classified balance sheet may include the following.

Each subheading includes various line items like the typical balance sheet. Companies may also choose to prepare the classified balance sheet using a two-sided approach. Consequently, they will put assets on one side and liabilities and equity on the other. Either way, the classifications within these headings will remain the same. ExampleGiven below is an example of a typical classified balance sheet.

What is the importance of the Classified Balance Sheet?The classified balance sheet provides companies with an alternative way of reporting their financial position. On top of that, it allows them to help investors and other stakeholders understand and analyze the information. Similarly, the classified balance sheet enhances ratio analysis by classifying related data. Compared to its traditional counterpart, the classified version provides significant advantages. The classified balance sheet also allows companies to provide more information to users than the traditional one. It helps explain various areas better, such as accrued and prepaid expenses, liabilities, fixed assets, etc. Although most companies use the traditional balance sheet, investors may prefer the classified one more. ConclusionThe balance sheet is a financial statement that reports on the financial position of an entity. While most companies prepare the standardized version of this statement, some prefer the classified one. The classified balance sheet provides better information on various subcategories while maintaining the essence of the accounting equation. Post Source Here: Classified Balance Sheet: Definition, Examples, Format, Template, Importance What is a 750 credit score? Is it good or bad? A 750 credit score is considered to be excellent, and it will allow you to qualify for the best interest rates and terms when borrowing money. However, even if your credit score is lower than 750, there are still steps you can take to improve your credit rating. In this blog post, we will discuss what a 750 credit score means for you and how you can achieve or maintain this high score. What does a credit score of 750 mean?A credit score is a number that lenders use to assess your creditworthiness. This number is based on your credit history and helps lenders determine whether you are a good candidate for a loan or line of credit. A high credit score means you have a strong history of making timely payments and managing your debt responsibly. Conversely, a low credit score may indicate that you have missed payments or racked up debt that you have been unable to pay off. Most credit scores range from 300 to 850, and a score of 750 or above is considered excellent. If your credit score is in this range, you will likely qualify for the best interest rates and terms when borrowing money. You may also be able to qualify for special perks, such as cashback rewards or airline miles, from some credit card issuers. How much can I borrow with a 750 credit score?If you have a credit score of 750, you will be able to qualify for loans and lines of credit with the best interest rates and terms. For example, if you are looking to take out a mortgage, you may be able to qualify for a lower interest rate than someone with a lower credit score. This can save you thousands of dollars over the life of your loan. If you are looking to finance a new car, you may be able to qualify for 0% APR financing. This means you will not have to pay any interest on your loan for a certain period of time, which can save you money in the long run. How to get a 750 credit score?If your credit score is below 750, there are still steps you can take to improve your creditworthiness. One of the best things you can do is to make all of your payments on time and keep your balances low. You should also consider signing up for a credit monitoring service, which can help you keep track of your credit score and identify any potential red flags. FAQsIs a credit score of 750 good for a home loan?Yes, a credit score of 750 is considered excellent and will allow you to qualify for the best interest rates when taking out a mortgage. What is the highest credit score possible?The highest credit score possible is 850. However, it is important to note that only a small percentage of people have a credit score this high. Is it hard to get a 750 credit score?No, it is not hard to get a 750 credit score. However, it is important to maintain good financial habits in order to keep your score high. What are the benefits of having a 750 credit score?Some of the benefits of having a 750 credit score include qualifying for the best interest rates on loans and lines of credit, as well as special perks from some credit card issuers. How can I maintain a 750 credit score?To maintain a 750 credit score, you should make all of your payments on time and keep your balances low. You may also want to consider signing up for a credit monitoring service. Is a 750 credit score enough to buy a house?Yes, a 750 credit score is considered excellent and will allow you to qualify for the best interest rates when taking out a mortgage. Is a 750 credit score good for a car loan?Yes, a 750 credit score is considered excellent and will allow you to qualify for the best interest rates when taking out a car loan. You may also be able to qualify for 0% APR financing. What is a good credit score?A good credit score is typically anything above 700. However, the definition of a "good" credit score may vary depending on your lender or financial institution. The bottom lineA credit score of 750 is considered excellent. If you have a credit score in this range, you will likely qualify for the best interest rates and terms when borrowing money. You may also be able to qualify for special perks, such as cashback rewards or airline miles, from some credit card issuers. To maintain a high credit score, you should make all of your payments on time and keep your balances low. You may also want to consider signing up for a credit monitoring service. If you have any questions about your credit score or how to improve it, we suggest speaking with a financial advisor. They can help you create a plan to improve your creditworthiness and reach your financial goals. Article Source Here: 750 Credit Score: Is It Good or Bad? Pairs trading is a market-neutral trading strategy that involves buying and selling two stocks simultaneously. The idea behind pairs trading is to find two stocks that are in co-movement and to take advantage of the differential in their price movement. In order for pairs trading to be successful, you need to find two stocks that are: - Highly correlated with each other - Have a strong historical relationship - Are in the same industry or sector Once you have found two stocks that meet the above criteria, you can begin to monitor their price movement. When one stock outperforms the other, you can take a long position in the stock that is outperforming and a short position in the stock that is underperforming. Most published papers generally conclude that pairs trading can be a profitable strategy if done correctly. Reference [1] presented, however, opposite results, Overall, the result shows that the Hurst method cannot generate a strategy that can outperform the market and its performance is superior as compared to the cointegration method but it is not as compared to the correlation method. This result does not correspond with the result of some other papers in the past, which states that the cointegration method is superior compared to other methods. On the other hand, the result implies that the market is efficient, so we cannot build a trading strategy and earn an excess return on the market, which corresponds with the efficient market hypothesis, though the question of whether the market is efficient or not still remains debated in the literature. Moreover, pair trading strategy in case of all methods can sometimes outperform the market in recession stage but cannot in the expansion stage, which confirms the market neutrality of pair trading strategy. In short, using the Hurst exponent method for selecting pairs, the authors concluded that pairs trading does not outperform Buy and Hold. This is contrary to the majority of publications. Let us know what you think in the comments below. References [1] Quynh Bui, Robert Ślepaczuk, Applying Hurst Exponent in pair trading strategies on Nasdaq 100 index, Physica A 592 (2022) 126784 Originally Published Here: Does Pairs Trading Deliver Alpha? If you're looking for a way to get money for school, you may have come across FFELP loans. But what are they? How do they work? And how can you get one? This blog post will answer all of your questions about FFELP loans and help you decide if one is right for you. What is an FFELP loan?So, what is an FFELP loan? FFELP stands for Federal Family Education Loan Program. It's a federal program that provides loans to students attending eligible colleges or universities. The loans are made by private lenders, but they're guaranteed by the federal government. That means if you can't repay your loan, the government will pay it back for you. There are two types of FFELP loans: subsidized and unsubsidized. With a subsidized loan, the government pays the interest while you're in school and during your grace period. An unsubsidized loan accrues interest from the time it's disbursed, but you don't have to make payments until after you graduate or leave school. The interest rate on an FFELP loan is variable, which means it can change over time. The current interest rate for subsidized and unsubsidized loans is 2.83%. How to apply for an FFELP loan?To apply for an FFELP loan, you'll need to fill out the Free Application for Federal Student Aid (FAFSA). This form will determine how much money you're eligible to receive in financial aid. Once you've received your FAFSA results, you'll need to contact the financial aid office at your school to apply for an FFELP loan. If you're approved for an FFELP loan, you'll need to sign a promissory note. This is a legal document that states you agree to repay your loan. You'll also need to complete entrance counseling, which is a session that provides information about your rights and responsibilities as a borrower. Once you've signed your promissory note and completed entrance counseling, your FFELP loan will be disbursed to your school. The school will then apply the money to your tuition and fees. If there's any money left over, it will be given to you in the form of a refund. If you have any questions about FFELP loans, be sure to contact the financial aid office at your school. They'll be able to help you determine if an FFELP loan is right for you and walk you through the application process. Benefits of FFELP loansThere are several benefits of FFELP loans. One benefit is that you can choose your repayment plan. There are six repayment plans to choose from, and you can change your plan at any time. You can also consolidate your FFELP loans, which can lower your monthly payment and save you money on interest. Another benefit of FFELP loans is that there are deferment and forbearance options available. Deferment allows you to temporarily postpone your payments if you're experiencing financial hardship. Forbearance allows you to temporarily lower your payments or extend the repayment period. If you're having trouble making your payments, you should contact your loan servicer. They may be able to help you lower your payments or put you on a repayment plan that's more manageable for you. Drawbacks of FFELP loansThere are also some drawbacks of FFELP loans. One drawback is that the interest rate is variable, which means it can increase over time. Another drawback is that there's an origination fee, which is a fee charged by the lender when you first take out the loan. FAQsWhat if I have a bad credit scoreIf you have bad credit, you may not be able to get an FFELP loan. And if you do get an FFELP loan, you may have to pay a higher interest rate. Will FFELP loans be forgiven?No, FFELP loans are not forgiven. However, you may be able to get your FFELP loan discharged if you meet certain criteria. Can I get an FFELP loan if I'm not a US citizen?No, you must be a US citizen or permanent resident to get an FFELP loan. What if I can't find a lender?If you can't find a lender, you can contact the Department of Education. They may be able to help you find a lender or direct you to other financial aid options. Is an FFELP loan a federal loan?Yes, an FFELP loan is a federal student loan. However, the lender is a private company. The Department of Education guarantees the loan, but the lender is responsible for disbursing and collecting the loan. Are FFELP loans covered under Navient settlement?No, FFELP loans are not covered under the Navient settlement. The Navient settlement only applies to FFELP loans that were serviced by Navient. If your FFELP loan was serviced by another company, it's not covered under the settlement. ConclusionFFELP loans can be a great way to finance your education. They offer several repayment options and deferment or forbearance if you're experiencing financial hardship. If you have questions about FFELP loans, be sure to contact the financial aid office at your school. They'll be able to help you determine if an FFELP loan is right for you and walk you through the application process. Article Source Here: FFELP (Federal Family Education Loan Program) Loans: What You Need to Know Fiat is a Latin word that translates to “it shall be” or “let it be done.” Fiat money or Fiat currency is a common term used to describe a government-issued currency that is not backed by a physical commodity. It lacks intrinsic value, and its value is based only on the faith that people have in it. A country’s currency is called Fiat money when its government has declared that it can be used as legal tender within that country. The United State dollar is an example of Fiat money. Definition of Fiat MoneyFiat money is a government-issued currency that is not backed by a physical commodity, such as gold or silver. Fiat money does not have intrinsic value and is used as legal tender. The value of fiat money is derived from the faith and credit of the issuing government entity. The United States dollar or American dollar is an example of fiat money. The United States issues currency and has legal tender laws in place that recognize the dollar as a valid form of payment for goods and services. Each country has its fiat currency, which is used as the primary form of payment within that country. In some cases, other countries may accept a foreign country's fiat currency as legal tender, but this is not always the case. How Does Fiat Money Work?Fiat money has purchasing power because the government has declared that it can be used to pay taxes. This creates a demand for the currency, which gives it value. Fiat money is also used as a reserve currency, which is a currency that other countries hold to pay for international debts. Fiat money is not backed by any physical commodity, so its value is not derived from anything tangible. The value of fiat money is based on faith, which is why it is also sometimes referred to as "faith-based currency." The government that issues fiat money can print as much of it as it wants, so there is always the risk of inflation. This happens when too much money is chasing too few goods, and prices go up. Fiat money is not backed by any physical commodity, so its value is not derived from anything tangible. Advantages and Disadvantages of Fiat MoneyFiat money has several advantages over other forms of currency.

However, fiat money also has several disadvantages.

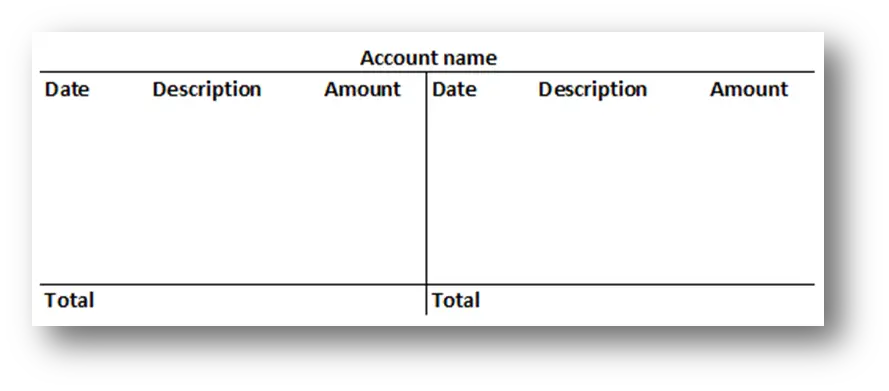

ConclusionFiat money has always been a major part of every country's economy. It's a government-backed currency that can be used to buy and sell goods and services. However, there is always the risk of inflation with fiat money as the government can print as much of it as it wants. Still, fiat money will be around for a long time and will continue to play an important role in the global economy. Originally Published Here: Fiat Money: Definition, Example, Meaning, Disadvantages and Advantages If you are a nurse, then you know that the field can be both challenging and rewarding. It is also a field that can be quite expensive to enter into, as tuition rates continue to rise. That's why many nurses turn to student loans to help finance their education. And once they complete their schooling and begin working in the field, they may qualify for nursing loan forgiveness programs. In this blog post, we will discuss what nursing loan forgiveness is, who qualifies for it, and what you need to do to apply. What is nursing loan forgiveness?Nursing loan forgiveness is a program that forgives a portion of your student loans if you work in certain qualifying fields for a certain period of time. For example, the National Health Service Corps Loan Repayment Program forgives up to 85% of your nursing school loans if you work in an underserved area for at least two years. To qualify for this program, you must be a U.S. citizen or national, have a bachelor's degree in nursing, and be licensed to practice in the state where you will work. If you are interested in applying for nursing loan forgiveness, there are a few things you need to do. First, you will need to research the different programs that are available and see if you qualify for any of them. Then, you will need to gather the necessary documentation and fill out an application. Once you have submitted your application, it will be reviewed by the program's administrators and you will be notified of their decision. If you are approved, then your loan payments will be forgiven over the course of the program. Who qualifies for nursing loan forgiveness?There are a few different programs that offer nursing loan forgiveness, so not everyone will qualify for each one. However, there are some general qualifications that most programs require. For example, you must be a U.S. citizen or national, have a bachelor's degree in nursing, and be licensed to practice in the state where you will work. Additionally, you will usually need to commit to working in a qualifying field for a certain period of time, such as two years. What are the requirements for nursing loan forgiveness?Each program has its own specific requirements, but there are some general things that you will need to do in order to apply. First, you will need to research the different programs that are available and see if you qualify for any of them. Then, you will need to gather the necessary documentation and fill out an application. Once you have submitted your application, it will be reviewed by the program's administrators and you will be notified of their decision. If you are approved, then your loan payments will be forgiven over the course of the program. Closing thoughtsNursing loan forgiveness can be a great way to help you pay off your nursing school loans. If you think you might qualify for one of these programs, be sure to do your research and apply today. Post Source Here: Nursing Loan Forgiveness: How to Qualify and What You Need to Know The accounting process involves various stages. The starting point within this process is a transaction. Once a company participates in this transaction, it must record it in the books of prime entry. Consequently, it reaches the general ledger, which helps prepare the trial balance and financial statements. The general ledger is the base for all accounting systems. Sometimes, companies represent general ledgers as T-accounts. What is a T-Account?A T-account is a presentation of the general ledger. As the name suggests, this presentation resembles the shape of the alphabet "T". A T-account includes two sides, a debit, and a credit. The left side is the debit, while the credit entries go on the right. The term T-account may also refer to the general ledger for a specific account within the financial system. The T-account presentation for the general ledger is often informal. Most companies use accounting software to create their records. Usually, this software prepares the account ledger in a traditional format. However, the T-account presentation is clearer and more concise. On top of that, it focuses on simplifying the general ledger with a visual impact. What is the format of the T-Account?As stated above, the T-account format resembles the alphabet "T". The line in the middle separates the debit and credit sides. For each side, the T-account includes at least three columns. These columns contain the date, description, and amount of the transaction reported. The top line holds the name of the account for which the company prepares the T-account. [caption id="attachment_6199" align="aligncenter" width="889"] At the bottom of the T-account, companies total the debit and the credit side. However, if one side exceeds the other, they must create a balance for the lower side. This balance will equal the difference between those sides. Once companies record the balancing figure, the total for both sides will match. This balancing figure will become the balance for the account in the trial balance. Some formats may omit the date column for both sides and aggregate transactions. However, the description and amount columns will remain. Usually, the description column includes the account name for the other side of the double entry. The amount column will only consist of the value for which this account is debited or credited. What is the difference between the T-account and General Ledger?Some people think the T-account and general ledger are different. However, the T-account is a visual representation of the latter. Both terms do not differ from each other. Sometimes, these terms may refer to the varying visual presentations used to present an account. Companies use T-accounts to represent general ledger accounts differently. In a traditional general ledger format, companies record transactions consecutively. This format includes the date, description, debit, and credit columns. However, it does not separate debits and credits on different sides. On top of that, companies record transactions as they occur in this format. However, the T-account segregates transactions into credit and debit sides. ConclusionGeneral ledgers are the base for preparing the trial balance and financial statements. Companies record transactions into different accounts in these records. Sometimes, they may use the T-account format to present these accounts. This format is straightforward and includes two sides, debit, and credit. Each side usually contains three columns, date, description, and amount. Post Source Here: T Account: Definition, Template, Accounting, Format, vs General Ledger If you are a veteran, you may be interested in learning more about VA life insurance loans. These loans offer veterans an opportunity to borrow money against the value of their life insurance policy. This can be a great way to get the money you need for any purpose, such as home repairs, medical expenses, or even debt consolidation. In this blog post, we will discuss how VA life insurance loans work and provide tips on how to get the best interest rates possible. What is a VA Life Insurance Loan?A VA life insurance loan is a type of loan that allows veterans to borrow money against the value of their life insurance policy. The loan is secured by the policy, which means that if you are unable to repay the loan, your life insurance policy will be used to pay off the debt. VA life insurance loans can be a great way to get access to cash when you need it, but it is important to understand how they work before you apply. How do VA Life Insurance Loans Work?VA life insurance loans are available through a number of different lenders, including banks, credit unions, and online lenders. The process for applying for a VA life insurance loan is similar to other types of loans. You will need to fill out an application and provide some basic information about yourself and your life insurance policy. Once you are approved for the loan, you will be able to borrow up to the cash value of your life insurance policy. The interest rate on a VA life insurance loan is typically lower than the interest rate on a traditional loan, and you will have up to 20 years to repay the debt. In most cases, you will make monthly payments on the loan, and the loan will be paid off when you die. If you have a surviving spouse, they will usually be able to keep the life insurance policy and use it to pay off the loan. How to Get the Best Interest Rates on VA Life Insurance LoansWhen you are shopping for a VA life insurance loan, it is important to compare interest rates from different lenders. The interest rate you qualify for will be based on your credit score and the value of your life insurance policy. In general, the higher your credit score, the lower the interest rate you will qualify for. You can compare interest rates from different lenders by shopping around and using an online loan calculator. If you are interested in taking out a VA life insurance loan, be sure to shop around and compare interest rates from different lenders. By doing your research and getting multiple quotes, you can be sure you are getting the best deal possible. What are the benefits of a VA life insurance loan?There are a number of benefits that come with taking out a VA life insurance loan. One of the biggest advantages is that you will be able to get the money you need in a short period of time. This can be helpful if you are facing a financial emergency and need access to cash right away. Additionally, the interest rates on VA life insurance loans are typically lower than the interest rates on traditional loans. This can save you money over the life of the loan. Another benefit of a VA life insurance loan is that it can be used for any purpose. This means you can use the loan to cover medical expenses, make home repairs, or even consolidate debt. The money you borrow against your life insurance policy can be used for any purpose you choose. What are the drawbacks of a VA life insurance loan?There are a few potential drawbacks to taking out a VA life insurance loan. One of the biggest risks is that you could lose your life insurance policy if you are unable to repay the loan. If you die before the loan is paid off, your life insurance policy will be used to pay off the debt. Additionally, the interest rates on VA life insurance loans can be higher than the interest rates on traditional loans. This means you could end up paying more in interest over the life of the loan. The bottom lineVA life insurance loans can be a great way to get the cash you need when you need it. However, it is important to understand the risks and benefits before you apply. By shopping around and comparing interest rates from different lenders, you can be sure you are getting the best deal possible. Additionally, be sure to understand the terms of the loan before you agree to anything. This will help you avoid any potential pitfalls and ensure you are getting the best loan possible. Originally Published Here: VA Life Insurance Loans: How to Get the Money You Need Most companies offer credit sales allowing customers to purchase goods and pay later. This process also involves a credit term that defines the time limit for the customer to repay their debt. Usually, customers settle these debts before that term. However, some customers may delay their payments. Companies may use dunning to demand customers pay their debts. What is Dunning in Accounting?Dunning is a business procedure often associated with accounting. It is when companies reach out to their customers to collect money from them. As stated above, this money relates to any goods or services provided to the customer in previous transactions. The intensity of this process may differ based on various factors such as customer history, credit terms, money owed, etc. Dunning often refers to aggressive methods used by companies to coerce customers into repayments. It is the reason it gets a negative reputation. Typically, dunning involves various steps beginning with gentle reminders, going to threats, or warnings. A method used in this process is sending customers a letter known as the dunning letter. What is a Dunning Letter?A dunning letter is a form of communication between companies and their clients. It involves sending a letter to a customer during the dunning process. Usually, it states that the customer must settle their overdue payments to the company. In the modern corporate world, companies have replaced the dunning letter with emails or other forms of digital reminders. The tone of a dunning letter may vary based on several factors, as mentioned above. These letters usually start with gentle reminders and may go to aggressive threats. Usually, a dunning letter follows a progression based on how stubborn the customers are in their settlements. However, it may have a limited impact after that. It is merely a part of the dunning process, which also involves other techniques. What are the types of Dunning Letters?In the past, most companies used a dunning letter that involved an actual letter sent through the mail. With time, other forms of communication have taken over this process. Some of the common types of dunning letters include the following.

The type of dunning letter used by a company may differ based on various factors. However, the underlying process and premise remain the same. How to write a Dunning Letter?There is no specific format that companies use for the dunning letter. The items included within this letter may differ based on various factors. Sometimes, companies have prewritten letters for different stages during the dunning process. The tone in these letters varies depending on how often and for how long customers delay payments. Usually, the dunning letter includes the following items.

ConclusionDunning refers to the process companies use to request settlements for previous transactions. This process may involve various forms of communication, including the dunning letter. Currently, companies use electronic or other methods to deliver these notifications. The dunning letter is crucial in reminding customers to settle their overdue balances. Originally Published Here: Dunning Letter: Definition, Meaning, Types, Sample, Template |

Archives

April 2023

|

T account format example[/caption]

T account format example[/caption] RSS Feed

RSS Feed