Derivative Valuation, Risk Management, Volatility Trading

|

It happened again, and again. Last Thursday volatility increased sharply at around 1.30 p.m, then it came back to normal at the end of day. For now, we ignore the cause. But this event reinforced our observation: sharp volatility spikes occur more and more frequently these days. [caption id="attachment_382" align="aligncenter" width="590"] In a low volatility environment like this one, market participants are becoming more and more aware of the potential risks caused by the volatility feedback loop which will happen when the short volatility players are forced to deleverage. Sharp spikes in volatility are usually caused by unanticipated, black swan type of events. According to Steve Cucchiaro, the following circumstances can have the potential of leading to black swans

Nobody knows when a black swan will happen. So the right question to ask is: how to protect oneself from the black swan events? We believe that using VIX options to construct ratio call spreads (for example 1x2 VIX calls) is a sensible solution. We note that recently, Joe Ciolli of Business Insider presented an example of a hedge against a massive increase in volatility. But according to his post, we think that the trade is risky, so this is not a good hedge.

Alternatively, the trade was constructed and executed correctly, but it was misinterpreted by the journalist. Originally Published Here: Potential Black Swans and How to Hedge Against Them

0 Comments

Quantitative trading has become a topic du jour lately. Many investors have been considering allocating more capital to quantitative funds. However, not all experts share the same opinion regarding the merits of quantitative strategies. There are even quants among the skeptics. Emanuel Derman is one of the most respected experts in the quant community. He spent 17 years as a lead quant at Goldman Sachs, and he is now a professor of financial engineering at Columbia University. He’s the author of 3 books: My Life as a Quant, Models.Behaving.Badly and The Volatility Smile. Derman found that, ...as physicists applied their expertise of the laws of motion, atoms and mathematics to investing, their models didn’t work nearly as well as they did in a lab. Newton’s law of gravity hasn’t changed for eons, Derman said, but human behavior in markets changes all the time, wreaking havoc on even the best models made by scientists.

In a recent Bloomberg article, Derman pointed out, “I’ve developed a lot of skepticism about anyone bringing their expertise from one field to another” ... “They say stocks are like atoms, or like genes. But stocks are not atoms or genes. There is a resemblance, but ultimately they are very different.” Read more Not only academics are skeptical, but also practitioners. For example DoubleLine Capital Chief Executive Officer Gundlach said that he doesn't believe in machines taking over finance. Another hedge fund manager doesn’t believe in backtesting models. ... according to Visser at Weiss Multi-Strategy Advisers, a $1.7 billion hedge fund in New York, human investors still have a big advantage when it comes to recognizing patterns and connecting the dots: Intuition. "The good thing about computers is that they don't have emotions," Visser said in a phone interview. "The bad thing about computers is that they don't have emotions. Computers can't detect human sentiment. They can't identify the usual suspects who typically attend crowded conferences when markets are at a top." Visser is particularly skeptical about all the money being spent on finding profitable trading strategies by testing them on historical data, or so-called backtesting. While that helps reveal how portfolios will likely perform under various market conditions, computers aren't yet adept at forecasting what people will do in the future, he wrote in a June paper. Read more So do quantitative trading models work? Let us know your opinions. Originally Published Here: Do Quantitative Trading Models Work?

We just pointed out additional reasons for the current low volatility. And yet, there are more!

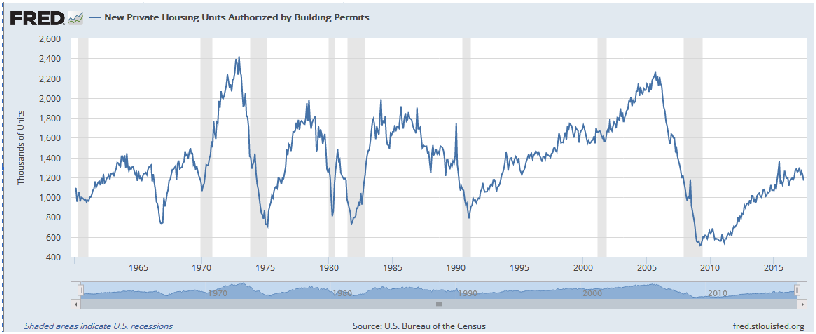

Some money managers are saying that passive investing has an effect of lowering the realized volatility. Sophie Baker reported: With the Chicago Board Options Exchange Volatility index, known as the VIX, hovering at the lower end of its 52-week trading range, these managers wonder if that isn’t a result of the increased popularity of passive investment strategies. “The move into passive investing has created an abnormal market environment,” said Paul Price, global head of distribution for Morgan Stanley (MS) Investment Management Ltd. in London. “The rush toward low-cost, but not low-risk, investing has resulted in the stock market rising and dipping together, greatly subduing stock volatility.” However, some money managers do not agree completely. Eric Lascelles, chief economist in Toronto at RBC Global Asset Management Inc., said passive investments generally mean fewer parties are actively working to set the right price for various financial vehicles. “I suppose it could indirectly support the thesis that the VIX is mispriced because of too many passive investors,” Read more Finally, as reported by Stephen Gandel, there exists a relationship between building permits and the volatility index.  ... the bears, and the bulls, may be reading too much into the the drop in volatility in part because of a surprising historical contributor. That’s where a new working paper published by the National Bureau of Economic Research this month comes in. The paper looked at the Great Depression, when stock market volatility, unlike today, was spiking. That coincided with a number of boom-and-bust building cycles. Gustavo Cortes of the University of Illinois at Urbana-Champaign, one of the paper’s authors, looked at more recent data, up through May, and found that the relationship still holds — when building permits are volatile, the stock market tends to follow suit. Recently, building permits have been relatively weak. The number issued nationwide, 1.2 million in May, has been trending down and is still way below where it was at the height of the 2000s building boom, when it peaked at 2.3 million a month. That could could make the low volatility a data point for the bears. Building permits have traditionally been seen as a leading economic indicator. Read more ByMarketNews Published via http://harbourfronttechnologies.blogspot.com/ Will this low volatility persist and can a large market decline happen in this environment? Aaron Brown recently published an article in which he pointed out that a large jump in realized volatility happens only when the VIX is above 20. ...the important thing is that there aren’t big surprises at low levels of the VIX. Realized volatility has never been above 20 percent starting from a VIX that is under 12 percent. And the really high realized volatilities are almost all starting from when the VIX is above 20 percent. This is consistent with our own studies. We observed that a large decline in the stock market happened only when the SP500 is below its 200-days moving average. In the past, there was only 1 instance when this was not true.

A. Brown concluded: ... both realized volatility and the VIX are at low levels, but not unprecedentedly low levels. Looking at what happened in the past starting from these VIX levels, it seems unlikely that we’ll get realized volatility above 20 percent at least over the next month. I’m not claiming a switch to a period of high volatility or a stock market crash is impossible. I’m saying that the evidence provides an argument that dramatic moves are unlikely anytime soon rather than a warning sign of an impending crisis. Read more From a qualitative point of view, Schroders chief economist and strategist Keith Wade thinks that this low volatility environment can persist for some time to come. He pointed out 3 main reasons for the subdued level of volatility:

The economist also noted: The next shock to markets may not be driven by the Fed, oil or China. It could be geopolitical in origin, for while political risks may have eased in Europe they are building in Asia where tensions between the US and China will rise if North Korea does not ease back on its nuclear weapons programme In summary, this low level of volatility can last for a while. And be careful when the VIX goes above 20.

Originally Published Here: How Long Will Low Volatility Last? |

Archives

April 2023

|

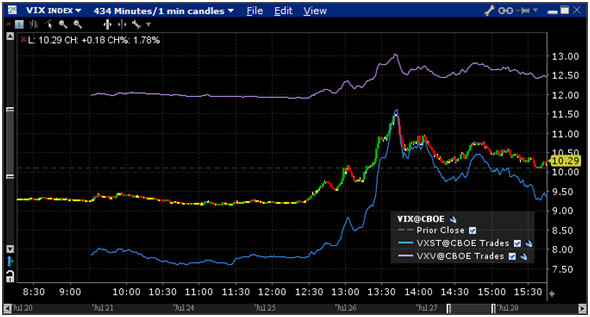

Volatility on July 27, 2017. Souce: InteractiveBrokers[/caption]

Volatility on July 27, 2017. Souce: InteractiveBrokers[/caption]

RSS Feed

RSS Feed