Derivative Valuation, Risk Management, Volatility Trading

|

In finance, beta measures a stock's volatility with respect to the overall market. It is used in many areas of financial analysis and investment, for example in the calculation of the Weighted Average Cost of Capital, in the Capital Asset Pricing Model and market-neutral trading. Beta of an investment is a measure of the risk arising from exposure to general market movements as opposed to idiosyncratic factors. The market portfolio of all investable assets has a beta of exactly 1. A beta below 1 can indicate either an investment with lower volatility than the market, or a volatile investment whose price movements are not highly correlated with the market. An example of the first is a treasury bill: the price does not fluctuate significantly, so it has a low beta. An example of the second is gold. The price of gold fluctuates significantly, but not in the same direction or at the same time as the market. A beta greater than 1 generally means that the asset both is volatile and tends to move up and down with the market. An example is a stock in a big technology company. Negative betas are possible for investments that tend to go down when the market goes up, and vice versa. There are few fundamental investments with consistent and significant negative betas, but some derivatives like put options can have large negative betas. Read more In this post, we present a concrete example of calculating the beta of Facebook, a technology stock. As for the market benchmark, we utilize SPY. The beta of a financial instrument is calculated as follows,

where

We downloaded 5 years of data from Yahoo Finance and implemented equation (1) in Python. The picture below shows the result returned by the Python program

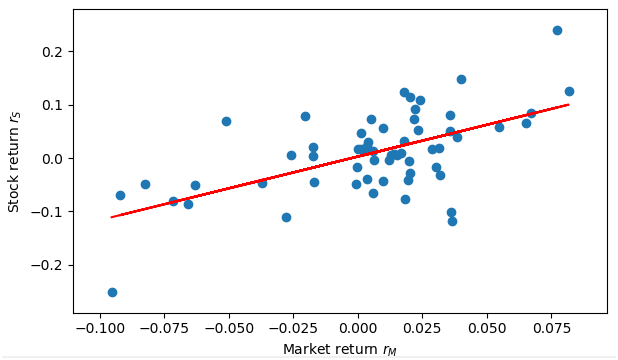

It’s observed that the beta of Facebook is 1.19, which means that Facebook is more volatile than the market. The next picture shows the stock returns regressed against market returns. Note that the slope of the linear regression line equals the beta of the stock.

Follow the link below to download the Python program. Article Source Here: What is Stock Beta and How to Calculate Stock Beta in Python

0 Comments

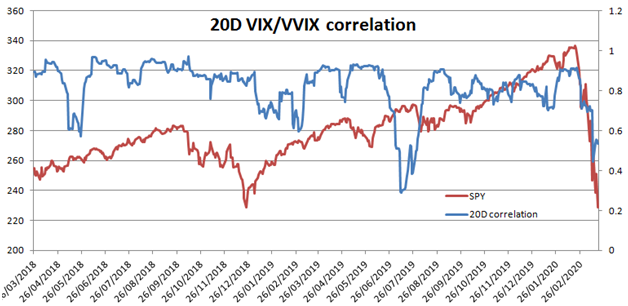

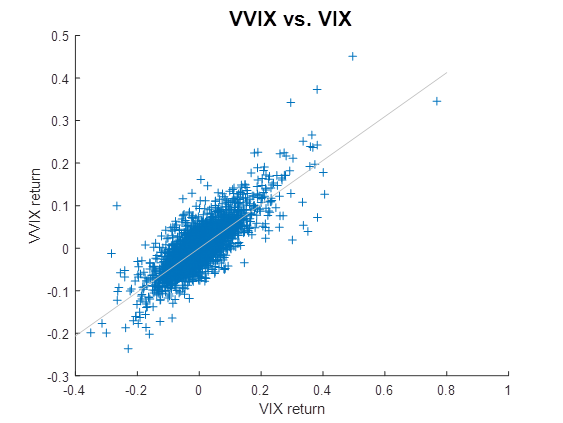

The VIX index is an important market indicator that everyone is watching. VVIX, on the other hand, receives less attention. In this post, we are going to take a look at the relationship between the VIX and VVIX indices. While the VIX index measures the volatility risks, VVIX measures the volatility-of-volatility risks. Its calculation methodology is similar to the VIX’s except that instead of using SPX options it uses VIX options. To study the relationship between these 2 indices, we first calculated the rolling 20-days correlation of the VIX and VVIX returns from January 2007 to March 2020. The median value of correlation is 0.807 and 25% quantile is 0.66 The figure below presents the rolling 20-days VIX/VVIX correlation for the last 2 years. We also superimposed SPY on the chart. We observe that the correlation is usually high but there are periods where it decreases significantly. The current period is one of those. [caption id="attachment_393" align="alignnone" width="628"] The next figure shows the scatter plot of VVIX returns vs. VIX returns. It’s observed that there is a significant population where VIX and VVIX returns are of opposite signs. We subsequently calculated the number of instances where VIX and VVIX move in the opposite direction. This indeed happens 22% of the time. [caption id="attachment_394" align="aligncenter" width="563"] Some implications of this study are:

See More Here: Correlation Between the VVIX and VIX indices Value at Risk (VaR) is a tool for measuring a portfolio’s risk. Value at risk (VaR) is a measure of the risk of loss for investments. It estimates how much a set of investments might lose (with a given probability), given normal market conditions, in a set time period such as a day. ... For a given portfolio, time horizon, and probability p, the p VaR can be defined informally as the maximum possible loss during that time after we exclude all worse outcomes whose combined probability is at most p. This assumes mark-to-market pricing, and no trading in the portfolio. For example, if a portfolio of stocks has a one-day 5% VaR of $1 million, that means that there is a 0.05 probability that the portfolio will fall in value by more than $1 million over a one-day period if there is no trading. Informally, a loss of $1 million or more on this portfolio is expected on 1 day out of 20 days (because of 5% probability). Read more There are basically 3 methods for calculating the VaR [1]

In this post, we implement the 3rd method, i.e. the Monte Carlo simulation, in Python. More details of the methodology can be found in Ref [1]. The simulation parameters are as follows,

We utilize 5-years daily data of SPY retrieved from Yahoo Finance. The picture below shows the VaR retuned by the Python program.

Note that the method presented in this post is suitable for calculating the VaR in a normal market condition. More advanced approaches such as Expected Tail Loss have been developed that can better take into account the tail risk. Follow the link below to download the Python program. References [1] Hull, John C. (2003). Options, Futures, and Other Derivatives. Prentice-Hall Originally Published Here: Value At Risk – Financial Risk Management in Python |

Archives

April 2023

|

Correlation between the VVIX and VIX indices[/caption]

Correlation between the VVIX and VIX indices[/caption] VVIX returns vs. VIX returns[/caption]

VVIX returns vs. VIX returns[/caption] RSS Feed

RSS Feed