Derivative Valuation, Risk Management, Volatility Trading

|

Derivatives are financial products whose values are determined by the current price of the underlying asset or portfolio. Weather derivatives are a particular class of financial instruments that individuals or companies can use in support of risk management in relation to unpredictable or adverse weather conditions. While some may see them as an exciting innovation, there is considerable debate about the future of weather derivatives and their suitability to specific situations. The main argument against them is that they are too complex and difficult to understand for the average person. Notably, the valuation of weather derivatives is not trivial as it often requires the modeling of an index whose forecast value can change drastically over the next few hours or days. We note that, There is no standard model for valuing weather derivatives similar to the Black–Scholes formula for pricing European style equity option and similar derivatives. That is because the underlying asset of the weather derivative is non-tradeable which violates a number of key assumptions of the BS Model. Typically weather derivatives are priced in a number of ways… [Index modelling] approach requires building a model of the underlying index, i.e. the one upon which the derivative value is determined (for example monthly/seasonal cumulative heating degree days). The simplest way to model the index is just to model the distribution of historical index outcomes. We can adopt parametric or non-parametric distributions. For monthly cooling and heating degree days, assuming a normal distribution is usually warranted. The predictive power of such a model is rather limited. A better result can be obtained by modelling the index generating process on a finer scale. In the case of temperature contracts, a model of the daily average (or min and max) temperature time series can be built. The daily temperature (or rain, snow, wind, etc.) model can be built using common statistical time series models (i.e. ARMA or Fourier transform in the frequency domain) purely based only on the features displayed in the historical time series of the index. A more sophisticated approach is to incorporate some physical intuition/relationships into our statistical models based on spatial and temporal correlation between weather occurring in various parts of the ocean-atmosphere system around the world (for example, we can incorporate the effects of El Niño on temperatures and rainfall). Read more Despite these difficulties, efforts are being made to price weather derivatives accurately. A recent paper [1] presents a valuation method for pricing an exotic wind power option using Monte Carlo simulations. Wind power generators face risks derived from fluctuations in market prices and variability in power production, generated by their high dependence on wind speed. These risks could be hedged using weather financial instruments. In this research, we design and price an up-and-in European wind put barrier option using Monte Carlo simulation. Under the existence of a structured weather market, wind producers may purchase an up-and-in European wind barrier put option to hedge wind fluctuations, allowing them to recover their investments and maximise their profits. We use a wind speed index as the underlying index of the barrier option, which captures risk from wind power generation and the Autoregressive Fractionally Integrated Moving Average (ARFIMA) to model the wind speed. This methodology is applied in the Colombian context, an electricity market affected by the El Niño phenomenon. We find that when the El Niño phenomenon occurs, there are incentives for wind generators to sell their energy to the system because their costs, including the put option price, are lower than the power prices. This research aims at encouraging policymakers and governments to promote renewable energy sources and a financial market to trade options to reduce uncertainty in the electrical system due to climate phenomena. References [1] Y.E. Rodríguez, M.A. Pérez-Uribe, J. Contreras, Wind Put Barrier Options Pricing Based on the Nordix Index, Energies 2021, 14, 1177. Originally Published Here: Pricing of Weather Derivatives Using Monte Carlo Simulations

0 Comments

Dividend yield is an input into the option valuation model that often receives little attention from the practitioners. This is probably because the majority of companies do not pay dividends. And for those that pay, an inaccuracy in the estimation of the dividend yield often has a small impact on the fair value of the financial instrument, especially if the tenor of the instrument is short. However, under some circumstances, dividend can become an important input in the valuation model, and an inaccurate estimation can lead to a severe financial loss. This is what happened with a French bank during the pandemic, The bank also lost about 100 million euros on dividend futures for the quarter, the people said. The losses had surged at one point to about 300 million euros before improving, according to the people. Dividend futures are derivatives that investors use to speculate on the payouts that companies make to shareholders. They have tumbled to historic lows in recent weeks as some of the world’s biggest corporations shred their awards in response to the coronavirus and, in some industries, pressure from regulators. Read more In this post, we discuss ways to determine the dividend yield accurately. In the option pricing model, the most accurate dividend yield is the implied one that can be calculated from

We’re not going to discuss dividend futures here as they are over-the-counter instruments and not traded frequently. Single stock futures, on the other hand, have been traded more frequently than dividend futures, but they are illiquid and the number of available single stock futures is still small. This leaves us with the last choice, i.e. using traded options to determine the implied dividend yield. Specifically, if the options are of European-style exercise, then we can use the put-call parity to create a synthetic single stock future, i.e.

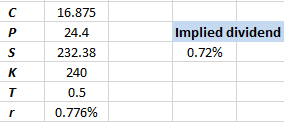

where C(K,t) is the call price at time t, P(K,t) denotes the put price, K is the strike price, S is the stock price, r is the risk-free rate, T is the time to maturity, and q is the continuous dividend yield. Note that equation (1) is model-free, and the implied dividend yield can be extracted easily by using it. This method has been implemented in an Excel spreadsheet.

As an example, we are going to calculate the implied dividend for Microsoft (MSFT) as of Feb-26-2021. The picture bellows shows the price of the 6-month call option with a strike price of $240. The price of the put option, as well as the risk-free rate, are provided in the Excel spreadsheet. The picture below shows the calculated implied dividend yield from MSFT traded option prices. We obtain an implied dividend yield of 0.72%.

Note that in the above example, for illustration purposes we assumed that the options are European style, but in fact they are American style, as is the case for most equity options. This means that the put-call parity no longer holds, and we cannot use eq (1) to calculate the implied dividend yield. Fortunately, there is a viable solution. Reference [1] presents a method that generalizes the put-call parity for the case of American options. Essentially, the author introduces a so-called early exercise premium into equation (1), thus allowing the generalized put-call parity relationship continues to be used in the calculation of the implied dividend yield. A novel element in this methodology is that it clears the hurdle of dealing with the early exercise premium that is not present in index options but is an element of value in American style options of US stocks. The Cox, Ross and Rubinstein (1979) binomial tree takes account of this premium and the tree is constructed simultaneously for a pair of put and call options with otherwise equal characteristics by guessing the same values for implied dividends and implied volatilities for the put and call pricing models. Analyzing dividends from stock options thus implied reveals their predictive power and adds to the understanding of cross-sectional stock returns.

Click on the link below to download the Excel spreadsheet. References [1] J, Kragt, Option Implied Dividends, https://ssrn.com/abstract=2980275 Article Source Here: How to Determine Implied Dividend Yield-Derivative Valuation in Excel Financial analysts study various companies to identify ones from which investors can benefit. Among these, there are two types of analysts. These include buy-side and sell-side analysis. Both of these are different in various aspects. Who are Buy-Side Analysts?Buy-side analysts are institutional investors who collect money from investors and invest it across various asset classes. They use different investing strategies to do so. A buy-side analyst seeks to determine whether an investment will be profitable and will fit the investment strategy. Once they do so, they can make recommendations to the investors for their funds. Buy-side analysts work to provide benefits to the funds that pay them. Therefore, they limit their recommendations to only the fund. For buy-side analysts, identifying the right investments is crucial for long-term success. It is because investors measure their performance based on whether the recommendations they make are profitable. Buy-side entities include hedge funds, asset management, institutional investors, private equity, ETFs, etc. The job of these institutions is to identify profitable investments for investors. For that, they identify relevant investments and gather information about them. Similarly, they use several models and techniques to gauge performance. Buy-side analysts also interact with sell-side analysts. They use reports generated by sell-side analysts to carry out further analysis of their own. While sell-side analysts will make their information available to the public, buy-side analysts don't. Similarly, buy-side analysts provide a more detailed analysis of the financial information for a specific purpose. Buy-side analysts involve analysts that require higher knowledge and skills than sell-side analysts. It is because they perform more technical analysis and provide better services to clients. However, that also means that they may come with higher costs to investors compared to other options. Who are Sell-Side Analysts?Sell-side analysts primarily provide unbiased recommendations based on the research they conduct on securities. They usually do so by following a list of companies within the same industry. It is different from buy-side analysts who follow stocks across various industries. Then they provide regular research reports to their clients. Similar to buy-side analysts, sell-side analysts also create models to forecast a company's financial results. Unlike buy-side analysts, however, they don't conduct the research at a high level. For sell-side analysts, the research reports and forecasts are the primary output. They also provide price targets and recommendations on how they estimate a stock will perform. The reports that sell-side analysts provide are available to the public. Therefore, anyone can use them according to their needs, which also includes buy-side analysts. However, they must create value for the services they provide for them to be successful. Usually, they do so by providing clients with comprehensive and detailed reports. Similarly, it may involve answering clients face-to-face. Sell-side analysts primarily include investment banking. However, it may also consist of commercial banks, stockbrokers, and market makers. These entities provide all the services mentioned above while also facilitating buying and selling of securities between investors. Essentially, the job of sell-side investors is to convince clients or act like marketers. ConclusionThere are various types of financial analysts in the market that may provide recommendations to investors. Buy-side analysts include entities that provide detailed analysis and recommendations to clients. They must make the right recommendations to stay successful. Sell-side analysts also make recommendations. However, these are not as detailed and are publicly available. Post Source Here: Buy-Side vs Sell-Side Analysts What is a Leveraged Buyout?A leveraged buyout represents a strategy that companies use to acquire other companies using debt as the primary source of finance. Leveraged buyouts may also include using the acquired company's assets as collateral to finance the transaction. Sometimes, however, companies may also use their own assets to obtain the debt for leveraged buyouts. Leveraged buyouts can be a hit or a miss for companies. Usually, it involves undertaking a significant amount of risk to finance these buyouts. Similarly, the acquiring company relies on the acquired company’s performance to repay the loan. Therefore, any problems within this plan can cause issues for the acquiring company. How do Leveraged Buyouts work?Leverage buyouts start when a company wants to buy out another company. As with any other transactions, they will need to finance the acquisitions. With leveraged buyouts, these funds come through debt rather than the acquiring company's equity. Therefore, companies may use a significant amount of debt to finance the transaction. Usually, leveraged buyouts involve a 90% ratio of debt while the rest comes from the acquiring company's equity. The acquiring company may issue bonds to acquire this debt. Due to the risk involved, however, the bond will be high-return rather than investment-grade. Leveraged buyouts usually include using aggressive tactics to acquire another company. Leveraged buyouts can occur through a company's current management or employees. Similarly, private equity firms may also participate in it. There may be several reasons for leveraged buyouts. These may include transferring private property, taking a public company private, or spinning-off a portion of an existing company and sell it. Similarly, companies may use leveraged buyouts to acquire a competitor and improve underperforming companies. Which companies are more prone to Leveraged Buyouts?Some companies are more prone to leveraged buyouts compared to others. These include companies that are in a mature industry. Similarly, companies that have stable and predictable earnings are better candidates for this purpose. It is because the acquiring company takes high risks on the acquisition. Therefore, having stability can help in repaying debts later. Similarly, companies with a strong team of personnel and involved in cost-cutting measures are prime candidates for leveraged buyouts. Acquiring companies also prefer target companies that have a clean balance sheet with minimal debt. Some other factors may also play a role in deciding whether companies will choose a target company for leveraged buyouts. What are the advantages of Leveraged Buyouts?Leveraged buyouts are advantageous to the acquiring companies. Through leverage, companies can finance acquisitions without having the equity necessary to do so. It also provides them with an opportunity to earn a higher return on investment. For some companies, acquiring underperforming companies and turning around can also yield significant returns. Leveraged buyouts can also be advantageous for sellers. The primary advantage is that sellers can dispose of their companies during their peak performance periods. This way, they can earn the maximum amount of money. Similarly, companies that are on the verge of failure or in a bad market position can also benefit from leveraged buyouts. ConclusionA leveraged buyout is the process of financing acquisitions primarily through debt. For the acquiring companies, it presents a significant amount of risk that they undertake to acquire finance. Leveraged buyouts can happen for several reasons. These can have various advantages for both the buyer and the seller, as mentioned above. Post Source Here: How Leveraged Buyout Works What is a Chief Financial Officer?A Chief Financial Officer (CFO) is a senior executive in companies, responsible for overlooking financial matters. In any company, a CFO is the highest rank figure in finance. Usually, CFOs are professionals with an understanding of financial matters and who can resolve any related issues. They also handle strategic-level financial decisions while delegating smaller tasks to others within the finance department. Chief Financial Officers usually include highly-qualified individuals who understand various aspects of finances. For example, they may include Master of Business Administration graduates or members of professional accounting bodies, such as CPA, CFA, Chartered Accountants, etc. Chief Financial Officers are also a director on the board of directors. CFOs usually report to Chief Executive Officers and the board of directors only. However, this is only one of the duties they perform. Apart from this, CFOs are also responsible for many other finance-related tasks in a company. What does a Chief Financial Officer do?The duties and responsibilities of a CFO in a company will differ according to the company’s requirements. Similarly, they may undertake some tasks while delegating others to junior-level staff. However, a typical Chief Financial Officer’s duties include the following. Financial ReportingReporting is the most crucial responsibility that CFOs perform. As mentioned, they are responsible for reporting performance to the CEO and board of directors. However, that is not all they do in this process. Chief Financial Officers are also responsible for preparing financial reports to report various aspects of a company. Almost every stakeholder a company has will be interested in the financial aspects reported in these statements. Financial ManagementCFOs are also responsible for managing the overall finances of a company. These may include overlooking its capital structure and how it obtains finances. Similarly, it includes managing its liquidity through working capital and cash management. In this role, CFOs are also responsible for overlooking the decision-making process related to new investments and projects. Strategic Decision-MakingBeing on the highest level of a company’s finance structure, CFOs are also responsible for strategic decision-making. Although most decisions go through the CEO, CFOs still play a significant role in them. Similarly, they influence the future direction that companies take with their finances. CFOs are also responsible for aligning a company’s finances with its strategies and facilitating growth. Risk ManagementCFOs are also responsible for risk management within a company. Each company will have its own risks due to its nature. These risks come with significant damages that can impact a company's business and its finances. Identifying and reacting to these risks is crucial for any company. The CFO assumes the responsibility for identifying these risks and mitigating them promptly. Legal and Regulatory ComplianceEvery company has to comply with various rules and regulations. If they fail to do so, they may face penalties and legal action. The CFO is responsible for identifying all applicable regulations and ensuring compliance. Similarly, CFOs are also responsible for compliance with all financial and tax rules relevant to the company. Financial AdvisoryA company's CEO is responsible for shaping the direction for the future. Due to this, they may make various decisions that they think will lead to long-term success. During this process, the CFO also plays a significant role. CFOs advise CEOs on how their plans can affect a company's finances. Likewise, the CFO is responsible for handling the finances for ensuring the strategies succeed. ConclusionChief Financial Officers are the ultimate finance authority figure in a company. These are individuals who have a high level of financial knowledge and skills. CFOs are responsible for overlooking a company's finances. Due to this, they may have various duties, as mentioned above. Originally Published Here: What Does A Chief Financial Officer Do Companies need to face various types of risks during their operations. Most of these risks accompany adverse implications for a company and cause damage to its operations. Therefore, identifying and dealing with these risks promptly is crucial for a company's success. These risks may come in various forms and from different sources. Among these, one of the most prevalent risks is operational risk. Before understanding operational risk management, it is crucial to look at operational risks. What is Operational Risk?Operational risks represent all uncertainties and hazards that companies face during their daily activities. These are uncertainties that come from within a company rather than outside of it. Since operational risks relate to a company’s operations, they might be different for each type of company or industry. Operational risks don’t necessarily need to result in losses. However, they can impact a company’s operations. Operational risk relates to the decisions that companies make and the procedures and processes in place. There are various sources from where these risks may come. For example, operational risks can come from product failure, health and safety issues, interruptions in processes, errors or omissions, litigation, etc. Identifying and managing operational risks is crucial for companies. What is Operational Risk Management?Operational risk management is a technique that companies use to manage their risks. These include processes and strategies that they put in place to identify and mitigate those risks. Operational risk management comes due to operational risks, such as internal processes failure, human errors, or external events. There are four principles included in an effective operational risk management framework. These include the following.

For many years, companies ignored operational risks and considered them trivial. These companies believe that operational risks depend on random variables occurring. However, more companies are putting emphasis on an effective operational risk management process. Through this, companies have taken a better view of their operational risks and managed them properly. Operational risk management starts with understanding a company's nature and the risks associated with it. As mentioned, these risks will differ according to the company's processes and operations. Once companies get an understanding of their operations, they can identify the risks associated with it. Similarly, they can design ways to manage and mitigate them. What are the benefits of Operational Risk Management?Operational risk management can have various benefits for companies. Firstly, these improve the reliability of business operations due to fewer failures. It also strengthens the decision-making process where companies face risks. Similarly, it lowers any costs associated with failures, for example, compliance costs. Operational risk management also reduces the overall impact or damage caused to companies. It improves the effectiveness of risk management operations with companies. It also allows companies to take a proactive approach to manage risks. It also comes with many other benefits for companies. ConclusionOperational risk relates to the issues that companies face during their daily activities. These stem from a company’s operations and can have an adverse impact on the company. Operational risk management is a technique used by companies to manage their risks. It involves identifying risks and managing them and can have many benefits for companies. Post Source Here: What Is Operational Risk Management When companies and businesses start operations, they may not be profitable. However, once they develop a customer base and good supplier relationships, they can earn more. These are things that come due to a company's reputation, often termed as goodwill. Developing a good reputation is crucial for a company's success in both the long- and short-term. However, companies may also damage their reputation sometimes. What is Reputational Risk?Reputational risk represents the dangers or threats that may damage a company’s goodwill. It comes from both internal and external factors. However, most commonly it stems from within a company and its operations. Companies may, as a result of their actions, create reputational risk. Similarly, a company’s employees may also give rise to reputational risk indirectly. Lastly, any entities that a company deals with can also tangentially affect its reputation. Reputational risks can create a lot of problems for a company. For example, it may result in a loss of customer base or good supplier relationships. It can also impact a company's revenues and profitability. Reputational risks can come from actions, such as security and safety issues, ethics violations, poor products or services quality, fraudulent activities, and much more. Regardless of the sources of reputational risk, companies can experience lower profitability. Sometimes, being associated with these activities even if they haven't committed such actions can cause issues. How does Reputational Risk work?The main impact of reputational risks on a company is on its goodwill. It is the relations and reputation that a company has accumulated over the past due to its operations. Companies may even have to pay additional money to reduce the impact on their reputation. Usually, companies that participate in activities that others may view as unethical face the highest reputational risk. However, companies don't need to participate in these activities directly to suffer due to reputational risk. It may also arise due to a company's employees behaving in their own interest or participating in unethical activities. For example, fraud within a company caused by its employees can result in reputational risk. Similarly, the relationships that companies develop can also bring harm to them. For example, if a company deals with a supplier that participates in unethical or fraudulent activities can also result in reputational risk. Likewise, companies may face this risk from their subsidiaries, joint ventures, and other related entities. Why is Reputational Risk crucial?Identifying and mitigating reputational risk is crucial for companies. Usually, companies can use various control measures to manage these risks. Due to the easier availability of information about a company's operations on the internet, reputational risk is more crucial than ever. Sometimes, these can result in instant implications, which may cause a lot of harm. Companies need to take a proactive approach toward reputational risk. Therefore, they need to identify the risks that can result in damage to their goodwill promptly. It is one of the risks where companies can benefit from preventing rather than controlling them. In case they fail to prevent reputational risk, they can face widespread implications. ConclusionReputational risk is crucial to a company's goodwill, which it develops through years of operations. Reputational risks can come from several sources. These may include a company's operations, its employees, or its associated parties. Companies need to identify these risks promptly and take a proactive approach to prevent them. Post Source Here: What Is Reputational Risk? Operational risk represents the risk that comes due to uncertainties and hazards in a company's operations. Operational risk is a type of business risk and can impact a company's profits adversely. This risk exists for every business and company. There are various operational risks that companies may face, one of which is a legal risk. What is Legal Risk?Legal risk consists of any uncertainties that companies may face due to fraudulent activities. It has various definitions. However, legal risks usually refer to any loss that companies may face due to their activities that may cause issues. For example, companies face legal risk due to defective transactions. Similarly, failing to take appropriate measures to protect its owned assets can cause legal risks. Legal risks may also refer to any risks that companies face due to changes in the laws. Legal risk is usually associated with operational risks as it may come as a result of fraudulent activity. Therefore, it can impact a company's operations and result in operational losses. Identifying different types of legal and operational risks is crucial for companies. It is because they will need to customize their responses to each risk. What are the various types of Legal Risk?Legal risks come from various sources. Usually, it comes as a result of the laws the apply to a company. For example, these may include employment laws, safety laws, tax laws, etc. Therefore, each type of legal risk may have a different impact on a company and its operations. Some of the types of legal risk include the following. AssetsAs mentioned, legal risks stem from a company's failure to protect its assets, whether tangible or intangible. Companies need to identify all their assets to identify and manage any risks associated with them. Once they do so, they can protect the rights and obligations related to all the legal assets owned by them. RegulationsRegulatory risks refer to any risks that companies face due to changes in regulations. For every company, identifying the applicable rules and complying with them is crucial. Regulatory risk is a type of legal risk and can impact a company's operations. Any changes in the legal implications and regulations can affect a company's operations and are, therefore, a part of legal risks. ContractsContract risk refers to the risks related to the contracts that companies undertake. These arise due to the failure of any of the two parties in an agreement to meet their obligations. Likewise, contract risks lead to legal implications for companies. Since it relates to a company's operations and legal matters, contract risks are a part of legal risks. DisputesWorking in a business environment gives rise to many duties. Due to these, companies may face various disputes. The risk of facing a legal dispute which also disrupts a company's operations is a part of legal risks. Even those that don't result in legal repercussions can lead to other risks such as reputational risk. ConclusionLegal risk refers to the uncertainties that companies face due to legal matters. Usually, it may relate to fraudulent activities within a company. Therefore, these are usually part of operational risks. Legal risks may come from various sources. These include assets, regulations, contracts, and disputes. Identifying the sources of legal risk is crucial in controlling and managing them. Post Source Here: What Is Legal Risk? There are various risks that surround any company. Some of these may come from external factors, while others may relate to internal operations. For external risks, there are five areas that may affect the risks faced by a company. These include political, economic, social, technological, environmental, and legal matters. Among the risks that come because of political and legal factors is regulatory risk. What is Regulatory Risk?Regulatory risk refers to any risk that comes due to changes in regulations or legislation. However, these risks are only worth protecting against if they affect a company or security adversely. Regulatory risks may impact a specific company or an industry as a whole. Following and satisfying all regulations is crucial in business success. Therefore, regulatory risks can result in an adverse change in a company. Regulatory changes come due to changes in laws or regulations. These changes usually come from a regulatory body. For example, for publicly-listed companies, the regulatory risk may come from changes in the stock market regulations. However, regulations may also relate to the government. Therefore, the policies of the jurisdictions in which a company operates are also relevant to regulatory risk. How does Regulatory Risk work?Companies and businesses need to abide by various rules and regulations to operate properly. These rules and regulations exist to direct them on how to function. In some cases, these may also exist to protect a company's stakeholders. For example, stock exchange rules and regulations help provide shareholders with security against fraudulent activities. For most regulations, not abiding by them is not an option. In case companies do not meet the specific requirements for each regulation, they may face penalties and legal action. Similarly, failing to satisfy them may also come with reputational risks. For example, customers may not be willing to transact with companies that do not follow environmental regulations. Overall, keeping track of regulations and meeting the requirements is crucial for companies. However, these regulations may also change from time to time. For example, governments may alter their policies, which can result in a change in regulations. Therefore, companies must ensure that they are aware of any regulatory changes that may affect them adversely. Companies usually have a risk management department that overlooks all these matters. This department follows all regulatory changes and ensures proper regulatory compliance. Similarly, the internal audit department may also track regulations and ensure the management complies with them. Although regulatory risks are not as common as others, they are still crucial and can impact a company's operations. Where does Regulatory Risk exist?Regulatory risks relate to changes in regulations that impact business activities. Usually, these risks are common for companies that follow a high number of regulations. For example, the regulatory risk may exist in the stock market due to the stock market regulations. Similarly, it is common for financial institutions to deal with these risks more than others. Regulatory risks can come from various sources. For example, changes in tax policy reforms each year can bring about regulatory risks with them. Similarly, changes in laws such as minimum wage laws can impact a business. ConclusionRegulatory risk is the risk that changes in regulations may adversely impact a company’s operations. For every company, identifying and complying with all regulations is crucial. However, these regulations may change with time and accompany adverse impacts. Regulatory risk is most common for companies that operate in a highly-regulated environment. Article Source Here: What Is Regulatory Risk? What is Corporate Governance?Corporate governance represents a system of rules, practices, and processes which dictate how companies should operate. Technically, corporate governance can be defined as "the system by which companies are directed and controlled in the interests of shareholders and other stakeholders”. The control and direction may come from within the company or from outside. Corporate governance provides a framework for achieving a company’s objectives. The purpose of corporate governance is to define a system that promotes transparency within a company. Similarly, it exists to provide security for a company's shareholders. Corporate governance became relevant due to various high-profile company failures in the past. Corporate governance also defines various committees that companies must have. One of these includes the audit committee that is essential for all companies. What is the Audit Committee?The audit committee is a committee that exists on a company's board of directors. It consists of independent non-executive directors. The primary function of the committee in a company is to provide evidence of increased accountability to shareholders. This committee is in charge of overseeing financial reporting and related disclosures. For most publicly-traded companies, having an audit committee is mandatory. For private companies, the audit committee must have at least one non-executive director. Public companies must have at least three independent non-executive directors. In either case, at least one director on the committee must have recent financial experience or qualify as a financial expert. The audit committee also coordinates with a company's auditors. Overall, the committee must include only independent directors. In case any of the non-executive directors on the committee cannot demonstrate independence, they cannot stay on it. The role of the audit committee in corporate governance is crucial for companies. What is the role of the Audit Committee in Corporate Governance?The audit committee in a company usually overlooks the financial matters. It includes any issues related to financial statements and auditing. During this, the audit committee plays a significant role in a company's corporate governance. Some of the primary functions that the audit committee performs in corporate governance include the following. The audit committee in a company evaluates critical issues and judgments that a company's management makes during financial reporting. It also reviews the effects of any accounting policies on a company's financial statements. The audit committee also ascertains that the company has appropriate policies and processes to identify or prevent fraud. Some regulations may require the audit committee to oversee the internal auditing function in a company. The committee also appoints, oversees, and compensates the independent auditor for a company. Overall, it acts as a liaison between a company's management and independent auditors. They also meet with both parties to discuss the audited financial statements. The committee also reviews non-financial information to ensure it relates to financial reports. Most companies also have a risk committee that overlooks a company's risk management process. In its absence, the audit committee also assumes the responsibility for risk management. Therefore, in some companies, it may be the audit and risk committee. Overall, the audit committee overlooks and controls a company's financial matters. Apart from the above roles, the audit committee can also look at compliance and regulation matters. Similarly, the audit committee may also perform several other finance-related duties in a company. ConclusionCorporate governance is a system of management through which companies are directed and controlled. Audit committees play a significant role in corporate governance. Usually, a company’s audit committee overlooks financial and audit matters. Similarly, it may also handle risk and compliance issues. Having an audit committee is mandatory for publicly-listed companies. Originally Published Here: Audit Committee Role in Corporate Governance |

Archives

April 2023

|

RSS Feed

RSS Feed