Derivative Valuation, Risk Management, Volatility Trading

|

Break-even analysis is a key concept in corporate finance that determines the point at which a company breaks even on its operations. It helps to determine the point at which total costs and total revenues intersect and is one of several measures of the company's financial performance. This analysis is frequently used by managers to set sales goals, as well as assess operational efficiencies and customer demand. In this article, we will be discussing what break-even analysis is, examples and how does it work. What is Break-Even AnalysisBreak-even analysis is a tool that helps managers assess a company's production and sale capacity, as well as its profit potential. The break-even point refers to the volume of sales needed for a company to generate enough revenue to cover all of its cash outlays, which include fixed costs, variable costs, and departmental expenses. As such, this analysis is used to determine the best prices for the company's products. It is also useful in determining how much product should be produced. Break-even analysis can be simple or complex, depending on whether one considers all of a company's expenses, including taxes and depreciation costs. This complexity arises because firms must estimate their future cash outlays based on present or historical data. How does break-even analysis workIn general, this analysis is used to assess a company's ability to meet its financial obligations and remain sustainable. To make this assessment, analysts and managers must first determine the total fixed and variable costs of producing and selling their products. They can then determine how many sales must be made for expenses to equal income by using the formula: Break-even point based on units Break-Even point = Fixed Costs ÷ (Sales price per unit – Variable costs per unit) Break-even point based on sales dollars Break-Even Point = Fixed Costs ÷ Contribution Margin Contribution Margin = (Price of Product – Variable Costs) Examples of break-even analysisLet's say, for example, that you own a local coffee shop. You know that your monthly fixed costs (rent, electricity, salaries) amount to $2,000 and that each cup of coffee you sell is priced at $3. And let's say it costs you $1 to produce each cup of coffee. How much coffee must you sell in a given month to cover costs Break-even point in units = $2,000/($3-$1) = 1000 cups of coffee Now let's find out the Break-even point based on sales dollars We have to figure out the Contribution margin first. Contribution margin = (Price of Product - Variable Costs) Contribution Margin = $3 - ($1/cup) = $2 per cup Break-even point in sales dollars = Fixed Costs ÷ Contribution Margin = 2000 ÷ 2 = $1000 The break-even points for this coffee shop are 1,000 cups of coffee or $1,000. ConclusionSo there you have it. In this article, we have talked about break-even analysis in corporate finance. As you can tell by now, the break-even point is the volume of sales required to cover all of a company's expenses. This is the point at which expenses equal income. Although we have discussed some very basic information here, this article should give you a good understanding of the concept. Article Source Here: Break-Even Analysis

0 Comments

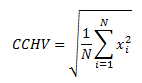

Mortgage refusals can be a stressful experience. You may have gone through the entire process of getting your mortgage pre-approved, and then receive a call from your lender saying that your mortgage has been declined. What went wrong? In this blog post, we will take a look at the latest mortgage refusal statistics and try to figure out why so many mortgages are being declined these days. Why are mortgages declined?There can be a number of reasons why your mortgage application might be declined. Your lender may have found some red flags in your credit history, or they may not think that you will be able to afford the monthly payments on the property. In addition, recent changes to mortgage rules and regulations mean that lenders are now required to take a closer look at your finances and make sure that you can actually afford the mortgage. What are the latest mortgage refusal statistics?According to a recent study by TransUnion, one in every ten mortgages was refused in 2017. This is up from one in fifteen mortgages that were refused in 2016. So what’s causing this increase in refusals? There are a few possible explanations. First of all, as we mentioned before, lenders are now required to take a closer look at your finances before approving your mortgage. This means that they are more likely to find something that could disqualify you for the loan. In addition, the study found that more people are applying for mortgages with alternative lenders, such as credit unions and private lenders. These lenders are often stricter when it comes to approving mortgages, so you’re more likely to be rejected if you apply through them. What can you do if your mortgage is declined?If your mortgage application is refused, don’t panic! There are a few things that you can do to try and get your mortgage approved. First of all, you can ask your lender for a letter of explanation. This letter will explain the reasons why your mortgage was declined, and it may help you to fix the issues that were found in your credit history. You can also try applying for a mortgage through a different lender. There are plenty of lenders out there, so you’re bound to find one that will approve your application. How can I improve my chances of getting my mortgage approved?There are a few things that you can do to improve your chances of getting your mortgage approved. First of all, make sure that you have a good credit history. Lenders will look at your credit score and make sure that you haven’t missed any payments or maxed out your credit cards. You should also try to save up a bigger down payment. This will show the lender that you’re serious about buying the property and that you’re not just trying to get a mortgage for the sake of it. Finally, make sure that you fully understand the terms of the mortgage. Lenders are now required to provide more information about mortgages, so make sure that you understand everything before you sign any paperwork. If you follow these tips, you should have no problem getting your mortgage approved. Just remember to stay calm if your application is initially declined – there are usually ways to fix the issue and get your loan approved. ConclusionIn this blog post, we looked at the latest mortgage refusal statistics and tried to figure out why so many mortgages are being declined these days. We found that one in every ten mortgages was refused in 2017, up from one in fifteen mortgages that were refused in 2016. There are a few possible explanations for this increase, including stricter lending rules and more people applying for mortgages with alternative lenders. If your mortgage application is declined, don’t panic. There are a few things that you can do to try and get your mortgage approved. First of all, you can ask your lender for a letter of explanation. You can also try applying for a mortgage through a different lender. Finally, make sure that you fully understand the terms of the mortgage. Originally Published Here: How Often Are Mortgages Declined? There are a lot of questions that go into whether or not real estate investment is a good idea. The first, and most important, question to ask is if you have the financial resources to invest in real estate. You need to have enough money saved up to cover your down payment, as well as additional costs that may come up during the buying process. Real estate investment is not a good idea for everyone. It's important to do your research and consult with a financial advisor before making any decisions. However, if you're willing to put in the effort, real estate investment can be a great way to build your wealth over the long term. This blog post will provide some guidelines for investing in real estate and help you decide if it's for you. What is real estate investment and why should you consider it?Real estate investment is the purchase of property with the intent to generate income, either through rental income, the sale of the property, or both. There are a number of reasons why you might consider real estate investment, including the potential for high returns and the ability to build equity over time. Before you make the decision to invest in real estate, it's important to do your research and understand the risks involved. Real estate investing is not a get-rich-quick scheme - it takes time, patience, and hard work to be successful. However, if you're willing to put in the effort, real estate investment can be a great way to build your wealth over the long term. How do you get started in real estate investment, and what are the risks involved?There are a few different ways to get started in real estate investment. One option is to purchase an investment property outright. This requires a significant amount of capital but can be a good way to get started if you have the finances available. Another option is to invest in a real estate investment trust (REIT). A REIT is a company that owns and operates income-producing real estate. When you invest in a REIT, you're essentially buying shares in a portfolio of properties. This can be a more affordable way to get started in real estate investment, and it's also a good way to diversify your portfolio. However, there are some risks involved with real estate investment. One of the biggest risks is that the value of your property could decline over time. This is especially true if you're investing in a single-family home or other types of property that isn't part of a larger development. Another risk to consider is the possibility of tenant damage. If your tenant damages the property, you may be responsible for covering the costs. Before making any decisions about real estate investment, it's important to talk to a financial advisor to get a better understanding of the risks and potential rewards involved. What are the benefits of real estate investment, and how can you make money from it?The potential benefits of real estate investment include the ability to generate income, build equity, and hedge against inflation. Real estate investment can be a good way to diversify your portfolio and reduce your overall risk. To be successful in real estate investment, it's important to have a clear strategy and understand the risks involved. It's not a good idea for everyone, and it's important to consult with a financial advisor before making any decisions. How does real estate investment compare to other types of investments, and is it a good idea for everyone?Real estate investment is a type of "passive" income - meaning you don't have to actively work to earn it. This can be a good way to generate income if you're looking for something that requires less work than a traditional job. However, it's important to remember that real estate investment is not a get-rich-quick scheme. It takes time, patience, and hard work to be successful. Real estate investment is also a good way to build equity. When you purchase an investment property, you're essentially buying a piece of property that has the potential to increase in value over time. This can be a good way to build your wealth over the long term. Finally, real estate investment can be a good way to hedge against inflation. As the cost of living goes up, the value of your property is likely to increase as well. This can help you keep up with the cost of living and maintain your purchasing power over time. Closing thoughtIs real estate investment a good idea for you? That depends on a few different factors, including your financial situation and risk tolerance. Before making any decisions, it's important to talk to a financial advisor to get a better understanding of the risks and potential rewards involved. Originally Published Here: Is Real Estate Investment a Good Idea? Internal controls refer to the rules and procedures within a company to ensure the integrity of financial and accounting information. These controls are essential to running a company. Similarly, they help with business continuity and ensure the accuracy of the financial reporting process. Internal controls are also a vital part of the auditing process. Auditors examine these controls through a test of controls. What is a Test of Control in Audit?A test of controls involves an evaluation of a client's existing controls performed by auditors. This test is relevant to both external and internal auditors. Usually, auditors use these controls to check the effectiveness of the existing internal controls. Furthermore, a test of controls can provide valuable insights into the strengths and weaknesses of those controls. Test of controls for internal auditing purposes helps companies identify weaknesses within internal controls. One of the primary tasks of an internal audit is to assess those controls. Usually, internal controls exist to detect or prevent risks of material misstatements. Therefore, a test of controls helps internal auditors establish whether the internal controls are sufficient in meeting those needs. What are the types of Tests of Controls in Audit?Auditors can use various audit procedures during a test of control. These procedures are known as the types or classifications of tests of controls. Usually, auditors choose the best procedure for a given client based on the circumstances. The types of tests of controls include the following. Examination or InspectionAn examination involves checking records or documents. For external audits, it may also include inspecting a tangible asset physically. This procedure allows auditors to determine whether the manual internal controls are operational. This process entails checking for authorization, signatures, stamps, etc. Usually, this type of test of controls involves reviewing written documents and records. InquiryInquiry is a procedure used within tests of controls that involves verbal examination. In this procedure, auditors ask the management and staff about the controls. However, an inquiry does not constitute high-quality audit evidence. Auditors use it along with the other types of tests of controls to gather sufficient appropriate audit evidence. ObservationObservation involves activities where auditors look at a process or procedure during its performance. Usually, it serves as evidence that the internal controls are operational. However, it only proves the internal controls worked during the observation time. Like inspection, auditors must use observation with other procedures to obtain better results. Re-performanceRe-performance is a type of test of controls where an auditor reperforms the internal controls. Usually, the auditor uses this procedure when the other classifications fail to produce sufficient evidence. Among the types of tests of controls, re-performance provides the highest assurance level. However, it may not apply to every internal control in place. When is a Test of Controls required?In external audits, auditors perform a test of controls after obtaining an understanding of internal controls. From the results obtained through this operation, external auditors conclude if they can rely on the client's systems. Consequently, they design audit procedures to assess the risks involved in the audit. Ideally, external auditors perform this process at the audit planning stage. While external auditors perform a test of controls as a one-off event, the same does not apply to internal audits. Internal auditors regularly execute various tests to assess the effectiveness of internal controls. On top of that, external auditors only utilize these tests to examine the impact on the financial statements. For internal auditors, the scope of tests of controls is broader. ConclusionA test of controls in audit refers to procedures used by auditors to assess a client's internal controls. It applies to both internal and external auditors. Usually, external auditors perform it during the planning or execution stage for an audit. However, it is an ongoing process for internal audits. There are several types of tests of controls that auditors may use. Post Source Here: Test of Control in Audit A stop-loss order is an order to buy or sell a security when the price reaches a certain level. A stop-loss order is designed to limit an investor's losses on a position in a security. There are two main types of stop-loss orders: stop market orders and stop-limit orders. A stop market order becomes a market order once the security reaches the designated price. A stop-limit order becomes a limit order once the security reaches the designated price. But is there any benefit of using stop-loss orders when trading securities? It is commonly believed that stop loss can help protect an investor's capital and avoid large losses on their investment. Reference [1] attempted to answer this question from a scientific point of view. It found that …even though stop-loss rules have poorer mean returns to a mean-variance optimal benchmark, they are effective at stopping losses. These rules reduce overall and downside risk, especially during declining market states. The transaction costs analysis shows that the significant effectiveness of risk reduction holds for these rules with larger stop-loss thresholds. This essay finds that stop-loss rules are an important factor of international equity allocation in a parametric portfolio policy setting. These rules generate portfolios with larger mean and risk-adjusted returns. This result is economically stronger in declining markets. The outperformance is robust once the transaction costs are accounted for. Essay three shows that stop-loss rules enhance the returns to stocks with lottery features. Individual investors have a strong preference for lottery stocks that typically have irregular enormous gains and frequent small losses. Stop-loss rules are useful at reducing losses and protecting gains from large price rises. This essay highlights that the sell signals of popular technical rules and time-series momentum rules are consistent with stop-loss rules, thereby effectively increasing the risk-adjusted returns of lottery stocks. These rules would have helped investors avoid instances of major historical drawdowns and are particularly beneficial in recessionary markets. Some rules are robust to the inclusion of transaction costs. In short, the finding was that stop-loss orders add value. We believe that adding stop-loss rules would make a trade more complex. Usually, a trade is a bet on the terminal distribution or price dynamics of the underlying asset. Adding stop-loss rules would introduce path dependency, thus making the analysis more complicated. We would prefer using no stop loss. In order to avoid catastrophic losses, one can always use options as a hedge or or trade options outright. Let us know what you think in the comment below. References [1] B. Dai, Essays on Stop-loss Rules, 2021, Massey University Article Source Here: Do Stop-Loss Orders Add Value? Historical volatility is a prevalent statistic used by options traders and financial risk managers. Historical volatility measures the past fluctuations in the price of an underlying asset. When there is a rise in historical volatility, a security’s price will also move more than normal. At this time, there is an expectation that something will or has changed. If the historical volatility is dropping, on the other hand, it means any uncertainty has been eliminated, so things return to the way they were. There are various types of historical volatilities such as close to close, Parkinson, Garman-KIass, Yang-Zhang, etc. We implemented the closed-to-close historical volatility in a calculator. The close-to-close historical volatility (CCHV) is calculated as follows,

where xi are the logarithmic returns calculated based on closing prices, and N is the sample size. In this example, N=22, the average number of trading days in a month. InputUse the dropdown menu highlighted in yellow to choose the stock. OutputThe calculator returns the following results

Check out other finance calculators on our website. Let us know what calculator you want us to develop in the comment section below. Article Source Here: Historical Volatility-Online Calculator A loan officer is someone who helps people get loans. They work with banks and other lending institutions to find the best loans for their customers. They help people apply for loans, and they also work with borrowers to make sure that they are making payments on time and that they are getting the most out of their loans. If you are looking for a loan, or if you want to become a loan officer, then this blog post is for you. Who is a loan officerA loan officer is a professional who helps individuals and businesses obtain loans. They work with banks, credit unions, and other lending institutions to help borrowers find the best possible loan products for their needs. Loan officers often have years of experience in the banking or financial services industry, so they can provide advice and guidance to borrowers on the best way to finance a purchase or investment. What does a loan officer do?Loan officers typically do the following:

A loan officer's main responsibility is to help borrowers find the best possible loan products for their needs. They meet with potential borrowers to discuss their needs and financial situation, evaluate applications for loans, recommend loan products, and negotiate the terms of loans with lenders. They also help borrowers understand the terms of their loans and ensure that all legal and regulatory requirements are met. How to work with loan officersLoan officers typically work for banks, credit unions, or other lending institutions. However, there is a growing number of freelance loan officers who work directly with consumers. If you're looking for a loan, it's important to work with a loan officer who is qualified and can help you find the best possible product for your needs. You can find a qualified loan officer by asking your friends and family for referrals, or you can contact the National Association of Mortgage Brokers or the American Bankers Association. When you're working with a loan officer, be sure to provide all the necessary information so that they can evaluate your loan application. This includes your credit score, income, and debt-to-income ratio. It's also important to be honest and upfront with your loan officer. If you're not sure about something, ask them for clarification. It's also important to keep in mind that a loan officer is not a financial advisor. They can provide you with information about different loan products, but it's up to you to decide whether or not a particular loan is right for you. How to become a loan officerThe best way to become a loan officer is to earn a degree in banking, finance, or economics. You can also obtain experience in the banking or financial services industry. Once you have the necessary skills and knowledge, you can become certified through organizations such as the American Bankers Association or the National Mortgage Licensing System and Registry. In summaryA loan officer is a professional who helps individuals and businesses obtain loans. They work with banks, credit unions, and other lending institutions to help borrowers find the best possible loan products for their needs. Loan officers often have years of experience in the banking or financial services industry, so they can provide advice and guidance to borrowers on the best way to finance a purchase or investment. Originally Published Here: Who is a Loan Officer and What Does He Do? When it comes to calculating insurance premiums, there are a lot of factors that go into the equation. Insurance companies take many things into account when setting rates, including the driver's age, driving record, and even credit score. In this blog post, we will break down some of the main factors that affect insurance premiums. We will also discuss how you can keep your rates as low as possible. The types of insurance and the premiums for eachThere are many types of insurance policies, and each one has its own premium. The main types of insurance are auto, home, health, and life. Here is a breakdown of the premiums for each:

Keep in mind that these are just averages, and your premiums may be different depending on the insurance company you choose. It is important to compare rates from different companies to find the best deal. You can use an online tool to get quotes from multiple insurers. The different factors that insurance companies consider when calculating premiumsThere are many factors that insurance companies consider when calculating premiums, including:

Keep in mind that these are just some of the factors that companies consider. Each company may weigh these factors differently, so it is important to compare rates from different insurers. How your age, gender, and marital status affect your premiumAge, gender, and marital status are all factors that insurance companies use to calculate premiums. Here is a breakdown of how each one affects your rates: Age: The older you are, the more expensive it will be to insure your car or home. Gender: Women typically pay less for insurance than men. Marital Status: Married people usually pay less for insurance than single people. Again, these are just averages, and your rates may be different depending on the insurance company you choose. How to get a discount on your insurance premiumThere are a few ways to get a discount on your insurance premium:

It is also important to note that some companies offer discounts for good drivers, so it is worth asking about this if you have a clean driving record. By following these tips, you can reduce your insurance premiums and save money. What to do if you feel like you're being overcharged for your insurance premiumIf you feel like you are being overcharged for your insurance premium, the first thing you should do is compare rates from different insurers. You may be able to find a cheaper policy with another company. You can also try negotiating with your current insurer. Many companies will lower your premiums if you threaten to leave. Finally, if you still feel like you are being overcharged, you can file a complaint with the Insurance Bureau of your state of residence Can bundling home and auto insurance lower the premium?Yes, bundling your home and auto insurance with one insurer can often lower your premium. This is because the company will be able to offer you a discount for having both policies with them. However, it is important to compare rates from different insurers to be sure you are getting the best deal. You may also be able to get a discount on your home insurance if you have a security system. Contact your insurer to find out more about the discounts they offer. ConclusionThere are many factors that go into the calculation of insurance premiums. To get the best deal, it is important to compare rates from different insurers and to maintain a good driving record and high credit score. You can also try bundling your home and auto policies with one insurer or increasing your deductible. If you feel like you are being overcharged, you can file a complaint with the Insurance Bureau of your state of residence. Thanks for reading! I hope this article was helpful. Please feel free to share it with your friends and family. Stay safe. Post Source Here: How Insurance Premium is Calculated: The Factors That Matter There is no one definitive answer to the question of whether or not it is a good time to buy a house for investment. It depends on a variety of factors, including your personal financial situation, the current state of the housing market, and your goals for the property. In this blog post, we will explore some of the pros and cons of buying an investment property at this moment in time. The current state of the housing marketOne of the biggest factors to consider when deciding whether or not to buy a house for investment is the current state of the housing market. Currently, the market is favor sellers rather than buyers, which means that it may be more difficult to find a property that meets your investment criteria. However, if you are able to find a good deal on a property, it could be a wise investment. On the other hand, if you are looking to sell your investment property in the near future, now may not be the best time. The current market conditions could lead to lower prices and less demand for investment properties. Overall, it is important to stay up-to-date on the current state of the housing market so you can make an informed decision about whether or not now is a good time for investment. The house buying process can be stressful and confusing, but it doesn’t have to be. There are many resources available online that will help guide you through this complex process from start to finish. In addition, it is always a good idea to consult with a real estate agent who can help you find the right property and navigate the housing market. The benefits of buying a property for investment purposes

The disadvantages of buying a property for investment purposes include:

How to find the right property to buyIf you are interested in buying a property for investment purposes, it is important to find the right one. You can do this by talking with real estate agents who specialize in your area or researching online at websites like Zillow and Trulia. Another option would be to consult with an accountant about what type of tax benefits might apply when purchasing an investment property. Factors to consider when making an investment decisionWhen looking for a property, it is important to consider the following factors:

There are many different types of investment properties to choose from, including single-family homes, condos, townhouses, and multi-unit dwellings. It is important to find one that meets your specific needs and investment criteria. The importance of having a solid financial plan in placeBefore buying a property for investment purposes, it is important to have a solid financial plan in place. This means having enough cash saved up to cover the down payment, closing costs, and any repairs that may need to be done. It is also important to have an idea of how much you can afford to pay each month in mortgage payments, as well as how much rent you can charge without putting yourself in a bind. Having a solid financial plan will help reduce the risk of buying an investment property that is not right for you. It will also help ensure that you are making wise decisions with your money and that you are on track to reach your long-term financial goals. ConclusionBuying a property for investment purposes can be a great way to build wealth over time. However, it is important that you do your research beforehand so you make sure this type of purchase fits within your financial plan and long-term goals. If you decide this is something worth exploring further then start looking at properties today. Article Source Here: Is It a Good Time to Buy a House for Investment? What credit card has the best rewards? This is a question that many people ask, but it is not an easy question to answer. There are many different credit cards available, and each one offers different rewards. In this blog post, we will discuss the different types of rewards that are available, as well as the best credit cards for each type of reward. We will also provide a list of the top 10 credit cards for rewards, so you can find the perfect card for your needs. What are credit card rewards?Credit card rewards are points, miles, or cashback that you earn when using your credit card. Rewards programs often vary by country and region, with some offering more generous terms than others. For example, American Express offers a variety of rewards cards in the United States, but only one type is available outside of North America: The Blue Cash Preferred® Card from American Express. What are the types of rewards?

What credit card has the best cashback?The answer to this question will depend on how much money you spend each month and where do most of your purchases take place. The best cashback credit cards usually offer a percentage of cashback on all purchases, as well as bonus rewards for spending in certain categories (such as groceries or gas). Some of the top cashback credit cards are the Chase Freedom Unlimited, the American Express Cash Magnet Card, and the Citi Double Cash Card. What credit card has the best travel rewards?The best credit card for travel rewards will depend on your individual needs and preferences. Some of the most popular travel rewards cards include the Chase Sapphire Preferred Card, the American Express Gold Card, and the Marriott Bonvoy Boundless Credit Card. These cards offer a variety of perks, such as airline miles, hotel points, and other benefits. What are the top ten credit cards for rewards?The following is a list of the top ten credit cards for rewards, based on our research. This list includes cashback, travel, and general rewards cards.

Closing thoughtWe hope this blog post has been helpful in answering your questions about the rewards programs available through various credit cards. Originally Published Here: What Credit Card Has the Best Rewards? |

Archives

April 2023

|

RSS Feed

RSS Feed