Derivative Valuation, Risk Management, Volatility Trading

|

When it comes to investing, investors have various options. Most commonly, investors prefer to invest in stocks or debt instruments. However, these investments do not represent a truly diversified portfolio of investments. Therefore, investors use techniques, such as asset allocation, to include other asset classes in their investment portfolios. One preferred type of investment for investors after stocks and debt instruments is real estate. Real estate represents any land and improvements on it, such as buildings, roads, fences, water, trees, etc. Usually, real estate offers two types of returns for investors. Firstly, it allows them to earn regular and steady income in the form of rent from tenants. On the other hand, it may also include property appreciation. What are the methods to valuing real estate?Investors interested in real estate investing can determine its value using three approaches. These include the income, sales comparison, and cost approaches. Each of these has some benefits and drawbacks. The income approach is complex and is similar to the discounted cash flow valuation method n finance. The income approach estimates a property's market value based on the income from it. Investors can calculate a property's value by discounting its future cash flows to its present value. There are two methods that investors can use for this process. These include the direct capitalization and yield capitalization method of valuation. What is the Direct Capitalization Method of valuation?The direct capitalization method of valuation comes under the income approach for real estate valuation. This method estimates a property's value by taking a single year's income forecast. Under this method, investors use the income recorded over time and dividing it by the capitalization rate for that period. Capitalization rate represents the rate of return that investors expect to generate on a real estate investment property. Investors can use the direct capitalization method of valuation in instances where a property generates income. In other cases, this method will not produce accurate results. It is because the income approach to valuing real estate relies on earnings produced from the real estate in consideration. This method differs from the yield capitalization method, which uses net operating income estimates for an investment holding period. What is the Direct Capitalization Method formula?Investors can calculate a property's value by dividing the net operating income from the property over the capitalization rate. Therefore, the formula for the direct capitalization method of valuation is as follows. Property Value = Net Operating Income (NOI) / Capitalization Rate For example, an apartment has a net operating income of $3 million. The capitalization rate is 5%. Therefore, the apartment’s value under the direct capitalization method will be $60 million. When do investors use the Direct Capitalization Method?Investors usually use the direct capitalization approach during two circumstances. Firstly, investors can use this method when the property in consideration is operating on a stabilized basis. For unstable properties, such as those with high vacancy rates, this method will not produce accurate results. Secondly, the direct capitalization method is also useful when there are enough similar properties for investors to estimate the capitalization rate. ConclusionInvestors looking for a diversified portfolio of investments usually consider real estate as a viable investment. Real estate includes land and any improvements on it. There are various approaches and methods of valuing real estate. One of these methods is the direct capitalization method. This method estimates a property's value by taking the net operating income and dividing it by the capitalization rate. Post Source Here: Direct Capitalization Method of Valuation

0 Comments

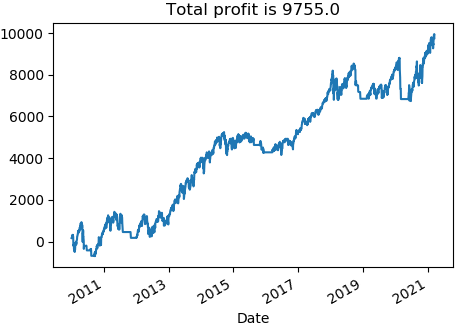

Investors often face the difficult decision of choosing between investing in commercial real estate vs residential real estate. Each of these investments has its own benefits and drawbacks. There are some differences between both of these that investors must understand. Before that, however, investors must understand what constitutes real estate and what it means. What is Real Estate?Real estate is a term used to describe property that consists of land, buildings, and other improvements. These improvements may include furniture and fixtures, utility systems, roads, structures, fences, etc. Real estate presents a diversified investment for investors and can be a crucial part of the asset allocation process. There are various types of real estate in which investors can invest, including residential and commercial real estate. What is Commercial Real Estate?Commercial real estate is any property used exclusively by businesses, such as companies, organizations, and other similar entities. Usually, these businesses can obtain commercial real estate through leases. The type of commercial real estate that each business uses will depend on its needs. There are several types of these properties, such as restaurants, hotels, stores, office space, malls, etc. What is Residential Real Estate?Residential real estate is any property used for residence purposes. These may include family homes, duplexes, mansions, condos, cooperatives, etc. Similarly, residential real estate is not available to businesses but only to individuals. These individuals can get the right to these properties through leases or acquiring them through mortgages. What are the differences between Commercial Real Estate and Residential Real Estate?There are many differences between commercial and residential real estate, some of which are as below. RisksInvestors face risks investing in both types of real estate. However, due to the stable nature of cash flows from commercial real estate, these risks are relatively lower than residential real estate. Residential real estate leases are generally short-term and favour the tenant. For that reason, residential real estate investments are relatively high-risk. ReturnsBoth commercial and residential real estate can provide decent returns for investors. However, commercial real estate returns are higher compared to residential real estate. It is mostly because investors can charge more rent per square meter for commercial property than residential real estate. On top of that, investors also have to account for maintenance costs for residential spaces. These are not usually an issue for commercial properties. Barrier of EntryDue to the lower prices of residential real estate, the barrier to entry is lower for investors. Usually, residential properties require less capital investment compared to other types of real estate. In contrast, commercial real estate has relatively higher barriers to entry. Besides, investors cannot obtain debt for commercial real estate easily due to the lower loan-to-value ratios for these properties. VolatilityBoth commercial and residential real estate investments provide investors to develop diversified portfolios. However, residential property usually performs better in times of economic downturns compared to commercial real estate. Commercial properties experience higher volatility due to businesses failing in economic crises. ConclusionReal estate represents any property that consists of land and improvements, such as buildings, furniture, and fixtures, utility systems, structures, etc. Investors can invest in commercial or residential real estate as a part of developing a diversified portfolio. However, both of these are different from each other. Residential real estate is different from commercial real estate in risks, returns, barriers to entry, and volatility, among other things. Article Source Here: Commercial Real Estate vs Residential Real Estate In a previous post, we demonstrated the mean-reverting and trending properties of SP500. We subsequently developed a trading system based on the mean-reverting behavior of the index. In this installment, we will develop a trend-following trading strategy. Trend following or trend trading is a trading strategy according to which one should buy an asset when its price trend goes up, and sell when its trend goes down, expecting price movements to continue. There are a number of different techniques, calculations and time-frames that may be used to determine the general direction of the market to generate a trade signal (forex signals), including the current market price calculation, moving averages and channel breakouts. Traders who employ this strategy do not aim to forecast or predict specific price levels; they simply jump on the trend and ride it. Due to the different techniques and time frames employed by trend followers to identify trends, trend followers as a group are not always strongly correlated to one another. Read more We continue to use simple moving averages as noise filters in order to generate buy and sell signals. Recall that the SP500 index is trending in the long term, therefore we will use a long-term moving average along with a shorter one. The trading rules are as follows, If 3-day simple moving average > 200-day simple moving average, buy $10000 worth of stock Exit if 3-day simple moving average < 200-day simple moving average We downloaded SPY data from Yahoo Finance and implemented the above trading rules in a Python program. The picture below shows the equity line of the strategy. We note that using the 3- and 200-day simple moving averages the strategy is overall profitable.

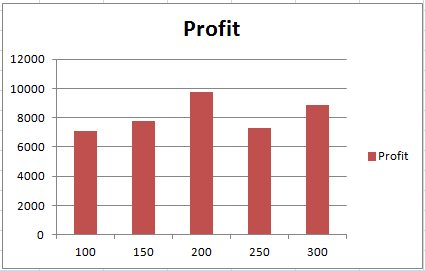

Next, we proceed to test the robustness of this system. To do so, we vary the length of the second moving averages (200 days in the above example). The graph below shows the total PnL as a function of the length of the second moving average. We observe that the overall profit remains positive when we change the length of the second moving average. This would indicate that the strategy performance is stable in this parameter regime.

In summary, we developed a simple trading strategy based on the trending property of the SP500 index. The strategy appears to be profitable and stable. Click on the link below to download the Python program and data files. Post Source Here: Trend-Following Trading System, Quantitative Trading in Python A derivative is a financial instrument that derives its value from an underlying asset or group of assets. This derivative usually comes in the form of a contract between two parties. Any movements in the underlying asset's value cause a fluctuation in the derivative's value as well. Derivatives may have various underlying assets, such as stocks, bonds, commodities, interest rates, etc. What is an Interest Rate Derivative?An interest rate derivative is a type of financial derivative that derives its value from movements in an interest rate or several interest rates. Interest rate derivatives are financial instruments most commonly used in hedging or speculation on interest rate fluctuations. Usually, these include financial instruments, such as futures, options, swaps, forwards, etc. Interest rate derivatives are prevalent among both individual, business, and institutional investors. All these parties use interest rate derivatives in some form to protect against the adverse effects of interest rate fluctuations. However, some investors may also use interest rate derivatives as a diversification tool or to alter their risk profile. How do Interest Rate Derivatives work?Interest rate derivatives help investors mitigate the risks associated with various debt instruments. These risks usually involve interest rate risks that come from market interest rate fluctuations. These derivatives also allow investors to speculate on the direction of future interest rate movements. Investors can either make profits from this speculation or use it to mitigate risks. Interest rate risks are inherent to any debt instrument that accompanies interest payments. These risks come as a result of any fluctuations in the market interest rates. Therefore, investors need to invest in an interest rate risk management process to mitigate these risks. For that, investors can use interest rate derivatives in various forms. What are the types of Interest Rate Derivatives?As mentioned, investors can use interest rate derivatives in various forms. Some of the types of interest rate derivatives are as below. Forward Rate AgreementsForward rate agreements are a type of interest rate derivate that investors use to protect against interest rate risks. Forward rate agreements allow investors to fixate interest rates in the future with a counterparty. This way, they can benefit from lower interest rates if the market interest rates rise in the future. Interest Rate OptionsInterest rate options are also a common type of interest rate derivatives that investors can use to mitigate interest rate risks. Interest rate options allow investors to speculate on the direction in which market interest rates will move in the future. Using this method, investors can either make profits from the speculation or protect their securities from interest rate risks. SwapsSwaps are a type of interest rate derivatives that allow counterparties to exchange their cash flows from debt instruments. There are two prevalent types of swaps that investors can utilize. These include interest rate swaps and credit default swaps. Usually, investors use interest rate swaps to exchange interest payments from floating rate instruments with fixed-rate ones. ConclusionInterest rate derivatives are financial instruments that derive their value from underlying interest rate movements. Interest rate derivatives allow investors to protect against the adverse effects caused by interest rate fluctuations. There are various types of interest rate derivatives that are prevalent in the market. These include, but are not limited to, forward rate agreements, interest rate options, and swaps. Originally Published Here: What is an Interest Rate Derivative? For investors involved in the bond or debt market, interest rate fluctuations can be critical. Usually, an increase or decrease in interest rates can affect the underlying security’s prices. It also constitutes the interest rate risk that investors face during their transactions. On top of that, interest rate risk is also crucial because it dictates how much premium a borrower has to pay to lenders for the provided finance. In most cases, investors can ignore interest rate fluctuations as these fluctuations may are temporary. Sometimes, however, the interest rates may change over the long term. In these cases, investors must mitigate the interest rate risk involved with their debt. The primary method that investors can use is to hedge against it. How to hedge Interest Rate Risks?Investors that receive fixed-rate interest on debt instruments will make a loss when the market interest rates increase. In contrast, those with floating rate interest instruments will experience favourable increases. If the market interest rates decline, the opposite will be true for both cases. With hedging, the primary objective will always be to protect investors against any losses. When it comes to hedging interest rate risks, investors have various options. For example, some investors may use forward contracts to mitigate the interest rate risks associated with their debt instruments. Similarly, investors also have the option to use futures or swaps to manage their risks. Each method of hedging against interest rate risks has its benefits and drawbacks. What is an Interest Rate Option?An interest rate option is a financial derivative that investors can use to hedge against interest rate risks. Through interest rate options, investors can speculate on whether the market interest rates will increase or decline. Investors can find these options on exchange in the form of different products. Interest rate options’ value depends on the underlying interest rate. Like most other options, interest rate options also come with two variants. These include call and put options. Interest rate options are also available over the counter. However, these are risky hedging options due to the strike price and expiry date of the option. What is the importance of Interest Rate Options?Interest rate options are one of the methods that investors can use to hedge against interest rate risks. Using these instruments, investors can speculate on the direction in which interest rates will move in the future. Using this method, investors can protect their investments against both short-term and long-term interest rate risks. Usually, investors need to perform several analyses to evaluate the direction in which interest rates will move. On top of that, interest rate options are prevalent in diversification strategies used by investors. Using these instruments, investors can diversify their portfolios to create a better position for themselves. Interest rate options aren’t only crucial for investors. Financial institutions, such as banks, can also benefit from them. ConclusionInterest rate risk occurs due to fluctuations in market interest rates. These fluctuations may affect the value of assets held by investors. Investors have various options that they can use to hedge against this risk. One of these includes interest rate options. Interest rate options are financial derivatives that allow investors to speculate on future interest rate movements. That way, investors can hedge against interest rate risks. Article Source Here: How to Hedge Interest Rate Risks? What is a Forward Rate Agreement (FRA)?Forward rate agreements are customized over-the-counter financial contracts. Through these agreements, two parties can predefine the interest rates for contracts that will commence in the future. One of these counterparties includes a buyer that borrows a principal amount at a fixed interest rate. The other is a lender that agrees to provide the loan at the specified time and rate. When both counterparties enter the forward rate agreement, they specify some terms for it. Usually, it includes the rate that will be applicable in the future, the notional value, and the termination date. After signing the contract, one party makes cash payments to the other. This payment represents the net difference between the contract’s interest rate and the floating interest rate in the market. How do Forward Rate Agreements work?A forward rate agreement involves two parties, known as the buyer and the seller. The buyer is the party that fixes the borrowing rate at the inception of the contract. The seller, on the other hand, sets the lending rate. At the contract's commencement, there is no profit or loss for both parties. However, this position changes as time progresses. The profit or loss that each party makes in a forward rate agreement depends on whether the market interest rates increase or decrease. Usually, the buyer benefits when the market interest rates increase compared to the fixed rate at inception. However, the seller also profits if the interest rate declines compared to the fixed rate at commencement. What is the purpose of Forward Rate Agreements?Forward rate agreements have many use cases. Usually, parties use FRAs to freeze their interest rate for the future. This way, they can protect themselves against any adverse impacts of interest rate fluctuations. For this to happen, the counterparty must agree to enter the agreement. However, the counterparty must believe the interest rates will go the opposite direction to benefit. What are the advantages and disadvantages of Forward Rate Agreements?There are various advantages for counterparties that use forward rate agreements. Most importantly, forward rate agreements allow investors to mitigate their interest rate risks. Investors use it for trading based on market participants’ interest rate expectations. For companies, forward rate agreements enable the use of derivative contracts that stay off-balance sheets. Furthermore, forward rate agreements allow parties to reduce future borrowing and lending risks. If an investor expects any adverse movements in interest rates in the future, they can use these agreements to protect themselves. This way, they can obtain certainty around their transactions in the future. However, these contracts can also beneficial to the opposite party. However, forward rate agreements involve the transfer of risks associated with future contracts to other parties. In these contracts, either the buyer or seller will bear the loss related to interest rate risk. Therefore, the counterparty risk associated with these agreements is high compared to other futures contracts. Forward rate agreements can also be challenging to close before maturity. What is a Forward Rate Agreement example?A company, Red Co., enters into a forward rate agreement with another company, Blue Co. In this agreement, both parties agree that Red Co. will receive a fixed rate of 4% on a nominal amount of $1 million. This interest will be one year from the contract date. The fixed-rate agreement will be 30 basis points lower than the set rate. In exchange, Blue Co. will receive the six-month LIBOR rate on the nominal amount determined in three years. As with all other forward rate agreements, this agreement is also cash-settled. The parties will make the payment at the beginning of the forward period after discounting the amount using the contract rate. ConclusionForward rate agreements are over-the-counter derivative contracts. Through these agreements, two parties can predefine the interest rate for a future contract. Any fluctuations in the interest rates in the future can cause profits or losses. Forward rate agreements can be highly beneficial for both parties. However, one party has to make a loss for the other to profit. Post Source Here: Forward Rate Agreement Example Credit risk is the risk associated with defaults from borrowers. In any debt transaction, the lender has to bear some credit risk associated with providing the loan. This risk depends on several factors, such as the borrower's past financial background, current earnings, security provided, etc. In case a borrower defaults on the loan, the lender has to incur significant losses. Therefore, each lender has to evaluate the credit risk associated with a loan before providing it. What is Credit Risk Analysis?Credit Risk Analysis is the process through which a lender analyzes the credit risk associated with their loans. It involves techniques and procedures through which lenders decide on whether to provide the borrower with credit or not. Usually, it involves a multi-step process that the lender carries out for every single borrower and loan transaction. The primary reason why lenders perform a credit risk analysis is to reduce the chances of default. This way, they can reduce the costs associated with the loan. Usually, credit risk analysis is a part of a lender's risk management and credit allocation process. There are various steps that lenders take during this process. It may include running background checks on the borrower, evaluating their income, examining their financial or bank statements, etc. How does Credit Risk Analysis work?The credit risk analysis process involves evaluating the credit risk involved for a specific borrower's loan. Usually, lenders perform various evaluations to measure a borrower's creditworthiness. It includes running credit checks on the borrower, such as background checks, financial history, earning reports, etc. Lenders may also assess the borrower's credit report for this information. Similarly, lenders may require employer letters for employed individuals applying for a loan. On top of that, lenders will also request bank statements. For businesses, lenders usually require their business plan or financial statements. Similarly, lenders may also ask the borrower to provide a credit reference. Furthermore, borrowers may also have to provide security during the process. Why do lenders perform Credit Risk Analysis?The primary purpose of performing credit risk analysis is to quantify the credit risk that each borrower presents to a lender. The credit risk analysis process usually includes measuring the probability of default for each borrower. Through this, lenders can assign measurable values to the default chances for every transaction. This way, the lender gets a quantifiable and comparable statistic for further processing. Furthermore, credit risk analysis is crucial in the decision-making process performed by lenders. Usually, lenders decide on whether to provide a loan to borrowers after performing a credit risk analysis. This process is also crucial for dictating the terms offered to borrowers. For example, a borrower with an undesirable credit risk will get higher interest rates compared to others. Every institutional lender has a credit analyst that performs credit risk analysis of its lenders. The primary purpose of this process is to evaluate a borrower's creditworthiness. While credit ratings are also a measure of creditworthiness, most lenders have switched to performing credit risk analysis in-house. This way, each lender can customize the process and get better results from the process. ConclusionCredit risk analysis is the process performed by lenders to assess the credit risk involved in a loan transaction. Based on this information, lenders can decide on whether they should provide a loan to a specific borrower. Credit risk analysis is of significant importance. The primary purpose of this process is to quantify a borrower's creditworthiness through several evaluations. Article Source Here: What is Credit Risk Analysis? Investors can use various hedging techniques to mitigate the risks associated with their equity and debt instruments. These techniques include the use of options, swaps, forwards, futures, etc. Usually, these use derivates, which are financial securities that get their value from an underlying asset or group of assets. One method of hedging through swaps is credit default swap. What is a Credit Default Swap?A credit default swap is a type of swap contract through which two parties swap their credit risk. Credit risk is the risk of a borrower defaulting on their payments on a given debt instrument. Through credit default swaps, investors can mitigate this risk by exchanging these risks with another party. For example, a lender can exchange the credit risk on their loan with another party if they think the borrower will default. A credit default swap provides the lender protection against defaults from a borrower. Through these swaps, the lender buying the instrument can shift their risk to the seller. Credit default swaps work similarly to insurance policies. The buyer gets protection against any unforeseen events involving their debt instruments. In exchange, the seller receives periodic payments from the seller. How do Credit Default Swaps work?Credit default swaps come into play when buyers expect the credit risk on their instruments to be high. For example, a company issues bonds in the market. A few individuals and other companies purchase these bonds. Later, one of the borrower companies expects the issuer to default on the loan. Therefore, the borrower can acquire credit default swaps to mitigate the risk. When the buyer purchases the credit default swap, the credit risk associated with the underlying debt instrument gets transferred. The swap seller agrees to bear this risk in exchange for regular payments from the buyer. This way, the buyer can mitigate the credit risk involved with the underlying debt instruments while the lender receives a steady income. In case the bond issuer defaults on the debt instrument, the credit default swap seller must compensate the buyer. This compensation will include both the principal and interest payments on the loan. Therefore, the buyer gets protection against any defaults from the issuer. In contrast, if there is no default, the seller will collect regular payments from the buyer as an income. What are the advantages and disadvantages of Credit Default Swaps?The most prominent advantage of credit default swaps is that it provides lenders protection against credit risk. Usually, these risks come from high-risk instruments that promise high rewards. It also allows the seller to protect themselves through diversification. For the seller, the credit default swap provides a regular source of income. However, credit risk swaps played a significant role in the 2008 financial crisis. It was primarily because of the unregulated nature of these swaps. Nonetheless, some regulations have been introduced for these derivatives since 2010. Similarly, credit risk swaps can be disadvantageous for the seller in case of default from the borrower. Credit default swaps can also cause lenders to invest in high-risk instruments, hoping the swaps would protect them against the risks. ConclusionCredit risk swaps involve the transfer of credit risk associated with an instrument to another party. Usually, the swap seller is a bank, insurance company, or financial institution that accepts this risk. Instead, the buyer makes regular payments to the seller. In case of default from the borrower, the seller has to compensate the buyer for the loan amount. Post Source Here: What is a Credit Default Swap? Who is a Credit Analyst?A credit analyst is someone responsible for evaluating the risk factors that affect loans and debts. Credit analysts are trained individuals who have a financial background in examining loan applications. They are different from loan officers who assist clients throughout the loan process. Instead, credit analysts examine a client's creditworthiness and background. The use of credit analysts during a loan process has become more prevalent in recent times. Credit analysts may work in financial institutions or credit agencies to carry out their tasks. Credit analysts collect critical financial information about a client and evaluate it using financial ratios and other techniques. What does a Credit Analyst do?Primarily, credit analysts examine a client’s creditworthiness through their past transactions. However, they also perform several other duties during the loan application evaluation process. Some of the roles and responsibilities that credit analysts perform are as below. Credit risk evaluationOne of the primary tasks that credit analysts carry out is evaluating a client's credit risk. They do so by examining their past savings information, earnings from various sources, debt repayment history, and other related dealings. Once they analyze this information, they can form an opinion about the client's creditworthiness using a credit rating. Client and product supportA credit analyst is also responsible for setting up meetings with existing and potential clients. The analyst is responsible for obtaining information on the client's financial background. The credit analyst also identifies the client’s needs and objectives for receiving the loan. Similarly, the analyst assesses the client’s earnings and spending capacity. Lastly, the credit analyst promotes credit lines and products to clients. Credit limit controlCredit analysts also review the credit limits for existing customers in case they want to increase their credit. The analyst will evaluate the borrower’s repayment history, default history, and earnings information to make a decision. Similarly, the credit analyst will make recommendations to the lender on whether to increase or decrease a client’s credit limit based on their dealings. Financial data analysisCredit analysts also analyze financial data related to potential and existing clients. It is one of their primary responsibilities. Based on this analysis, credit analysts can make decisions about clients. Usually, credit analysts use various financial ratios to determine their suitability for credit terms. The credit analyst also examines the client’s risk levels to evaluate their credit risk. Assisting the managerCredit analysts also assist the manager before approving a client. Usually, they do so to ensure the client meets some requirements for obtaining credit. These include collecting information and processing files, contacting other financial institutions to verify information, examining clients' assets and finances, etc. The objective of these checks is to help in the decision-making process. Record maintenanceCredit analysts are also responsible for maintaining detailed records relating to clients. Credit analysts ensure they have an accurate and up-to-date list of the annual reviews required by credit regulations. Similarly, they handle records related to the progress of new client applications and those already approved. Credit analysts also prepare monthly and quarterly credit reports. ConclusionCredit analysts are trained individuals who have a prominent role in a loan application process. These individuals evaluate risk factors that affect loan and debt applications. Similarly, credit analysts perform various duties in an institution. These include credit risk evaluation, client and product support, credit control limit, financial data analysis, assisting the manager, and record maintenance. Post Source Here: What Does a Credit Analyst Do? The term risk represents any chance or uncertainty that an outcome will differ from the expected outcome. Usually, any scenario that consists of uncertain possibilities that can result in losses constitutes the risk for that scenario. There are various types of uncertainties that investors can face according to their active market. One type of risk that is prevalent in debt markets is interest rate risk. What is Interest Rate Risk?Interest rate risk represents the uncertainty revolving around the interest rates prevalent in the market. For investors who are active in the debt market, an increase or decrease in interest rates can be critical. Therefore, interest rate risk also refers to the probability that unexpected fluctuations in interest rates may cause a decline in the value of an investor's asset. Usually, interest rate risks are common in bond markets or other fixed-income investment markets. For investors that receive interest on fixed-rate investments, a decline in interest rates is favourable. That is because these investors benefit from an increased earning while the market rates are down. In contrast, an increase in interest rates can be adverse as it means reduced earnings for these investors. On the other hand, for any party paying interest on loans, the opposite applies. An increase in market interest rates means the party pays lower interest than the market. Contrastingly, a decrease signifies the party pays higher interest than the market. On top of these losses, investors also make losses on the price of the security they hold. Usually, fluctuations in interest rates also cause the security’s price to alter. How does Interest Rate Risk affect security prices?As mentioned, the price of various bonds and debt instruments fluctuates with fluctuations in interest rates. Usually, when the interest rates in the market increase, a fixed-income bond or security will experience a favourable price increase. In these circumstances, most floating-rate interest securities will undergo a price increase. Furthermore, the maturity period of a debt instrument will also play a substantial role in how the prices will affect it. It is because instruments with a longer maturity will undergo fluctuation longer than an instrument with a short maturity. The longer the maturity period of the bond instrument is, the higher movement it will experience. At maturity, the market price and face value of the bond will equalize. How do investors manage Interest Rate Risks?For investors managing interest rate risks is crucial for long-term success. In some circumstances, investors may not have to take any action against fluctuations in interest rates. Usually, these changes are short-term, but some fluctuations may also be long-term. Therefore, investors need to monitor their securities to identify the risks. Investors have several options when it comes to managing interest rate risks. Usually, investors can choose from forwards, forward rate agreements, futures, swaps, options, embedded options, etc. Using these, investors can hedge the interest rate risks associated with their debt instruments. Most of these techniques involve transferring the risk to another party. ConclusionInterest rate risk is the risk involved with instruments that generate interest payments or receipts. Interest rate risks represent any uncertainty around interest rates prevalent in the market. Since any fluctuations in interest rates can affect security prices, investors need to manage their risks actively. Originally Published Here: What is Interest Rate Risk? |

Archives

April 2023

|

RSS Feed

RSS Feed