Derivative Valuation, Risk Management, Volatility Trading

|

Companies have several financial statements that report various aspects of their business. Among these, the balance sheet presents the assets and liabilities balances that companies own or owe. However, these do not contain all of those assets or liabilities. It is because some of these items may remain off the balance sheet. Off-balance sheet accounting has long been a debate topic for most experts. What is an Off-Balance Sheet?Off-balance sheet represents items that do not appear on a company’s balance sheet. It may include both assets and liabilities. However, that does not mean that companies don’t own these. Instead, some accounting standard provisions may disallow these companies from reporting them. In some cases, companies may also use it adversely and structure their assets and liabilities to stay off the balance sheet. Off-balance sheet accounting, while permissible, can also lead to some problems. For a company's stakeholders, off-balance-sheet accounting can cause incorrect decision-making. In some cases, assets and liabilities may miss the definition set by the contextual frameworks. Therefore, companies cannot disclose them. However, some companies may deliberately choose to keep items off-balance sheets to mask their financial health. What are Off-Balance Sheet Assets?Off-balance sheet assets are resources that companies may remove from their balance sheet. Despite them not appearing on the balance sheet, it does not imply that companies don't own these assets. Companies may hold these assets, whether tangible or intangible, but not report them on their balance sheet. Some companies may use it to their advantage and remove any assets that may have an adverse effect on their balance sheets. According to the contextual framework, assets are resources that companies own or control and result in future economic inflows. Any item that does not meet the definition cannot be a part of the balance sheet. There are some items that may not meet this definition. Therefore, it may give rise to off-balance-sheet assets that companies do not report. As mentioned, however, some companies may use it to benefit or mask their accounts. They may structure their assets, so they don't meet the definition and stay off their balance sheet. Inherently, off-balance sheet items are not deceptive in nature. However, companies may use them with the wrong intent, making them a problem for their stakeholders. An example of a company using off-balance-sheet assets is Enron. The company worked on assets and immediately claimed the projected profits from it. If the actual profits were lower than anticipated, it would remove the asset from the balance sheet. What are the types of Off-Balance Sheet Assets?There are various types of off-balance sheet assets that companies may keep away from their balance sheet. These include the following. Accounts ReceivablesWith accounts receivable balances, companies have the option to outsource their collection using a factoring company. Once they do so, they can remove the accounts receivable balance from their balance sheet. This way, they can outsource their default risk while also keeping the asset off their balance sheet. Operating leasesOperating leases come with an underlying asset that companies can use. However, their accounting treatment may require companies not to report the leased asset and the associated liability. In that case, companies only report the rent payments while keeping the asset away from the balance sheet. ConclusionOff-balance sheet items include any assets or liabilities that do not appear on a company's balance sheet. Off-balance assets are resources that a company may own but not report on its balance sheet. While the requirement to avoid including them may come to accounting standards, some companies may also use it adversely. Post Source Here: Off-Balance Sheet Assets

0 Comments

What is an Off-Balance Sheet?Off-balance sheet items include assets or liabilities that do not appear on a company’s balance sheet. However, that does not mean that these items may not exist. These are the actual assets and liabilities that companies own. However, there are some technical aspects that prevent them from appearing on the balance sheet. Off-balance sheet accounting has long been a critical point for experts. Most accounting standards have introduced provisions that prevent such accounting. Sometimes, however, off-balance sheet accounting may be necessary to meet the fundamental definition of elements. For example, operating leases in the previous accounting standards were off-balance sheet items. The latest accounting standards change that. What are Off-Balance Sheet Liabilities?Off-balance sheet liabilities are similar to any off-balance sheet items. These are obligations that companies may owe to other parties. However, accounting standards may not allow them to be a part of the balance sheet. Usually, companies and businesses don't need to perform any accounting treatment for these liabilities or report it in their financial statements. Usually, off-balance sheet liabilities include items that are not firm obligations. However, companies may need to settle them at a future date. For example, lawsuits may cause off-balance sheet liabilities where the company may need to pay it in the future. However, at the time of the reporting, the liabilities may not have realized. Despite that, most accounting standards require companies to disclose liabilities that may not appear on the balance sheet. There are various disclosure requirements for each liability that companies must follow. For example, reporting companies must disclose the possibility and nature of the lawsuits that are off-balance sheets. These may also be a part of the contingencies and commitments that companies report. Some companies may also use off-balance sheet accounting to keep their liabilities away from their financial statements. This kind of accounting is not permissible under most accounting standards. Companies do so to mask the financial position and appear more financially healthy. For some companies, it may be a case of removing any adverse liabilities to appear more liquid. What are some examples of Off-Balance Sheet Liabilities?There are various types of off-balance sheet liabilities that companies may have. Some of the most common ones include the following. Operating leasesFor a long time, operating leases have been a part of off-balance sheet liabilities. As mentioned, the latest changes in accounting standards may rectify it but with a limited scope. With operating leases, companies only report the associated rent payments. They do not list the asset or the liability that corresponds to the lease. Leaseback agreementsAs with operating leases, companies do not put leaseback agreements on their balance sheets. These agreements are common where one company sells an asset and leases it back from the buyer. Companies may use it to keep their financial statements clear of any adverse liabilities. Like with operating leases, companies don’t report the asset or liability associated with the agreements. They only record and report the related rent payments. ConclusionOff-balance sheet is a term used to describe assets or liabilities that companies have but don’t appear on their balance sheet. Off-balance sheet liabilities are the liabilities that companies may have to settle in the future but don’t report in the financial statements. Despite that, they must disclose it in the notes to the financial statements, as required by accounting standards. Originally Published Here: Off-Balance Sheet Liabilities A special-purpose entity (SPE) is a subsidiary company created by a parent company to isolate financial risk. This entity is legally separate from the parent company. It aims to absorb risks that the parent company faces. In some cases, SPEs can hold assets if the parent company enters bankruptcy. Another name used for a special-purpose entity is a special-purpose vehicle (SPV). SPEs have their own assets and liabilities. Similarly, investors can buy their stocks, which are legally separate from the parent company. SPEs may not be a part of the parent company’s financial statements or accounting record. However, there are some specific account criteria that they have to meet first. How does a Special Purpose Entity work?SPEs start with a parent company that creates the entity to isolate its assets or liabilities. Some other companies may use these entities to securitize their assets in case of bankruptcy. However, SPEs stay off the parent company’s balance sheet. Usually, companies create these entities when investing in risky projects to protect the parent company from the associated risks. In case the risks realize, the parent company always stays clear of any consequences. Since most SPEs remain off the balance sheet, the parent company does not suffer due to it. However, there are only particular cases where the use of these entities might be relevant. For example, special-purpose entities may serve as a counterparty for swaps and other similar credit-sensitive derivative instruments. SPEs may come in different forms, such as corporations, limited partnerships, trusts, etc. It usually depends on the parent company’s preference. However, they may also be helpful in creating joint ventures or performing financial transactions. Similarly, SPEs may come as either on- or off-balance sheet entities. What are the advantages of a Special Purpose Entity?SPEs can have various advantages. Firstly, it allows parent companies to isolate the financial risk associated with an investment. The parent company usually doesn't have to disclose these entities on their balance sheets, given they meet some conditions. Therefore, it allows companies to mask investments or projects from competitors or even investors. SPEs are also helpful in tax saving and planning. Usually, there is not much effort involved in creating these entities, making them easier to set up and use. Overall, SPEs allow parent companies to perform high-risk transactions. In case of failure, however, the parent company does not suffer the consequences. What are the disadvantages of a Special Purpose Entity?SPEs have several disadvantages. Parent companies can use these entities to mask information from stakeholders, which is not ethical in some cases. On top of that, they require a significant capital investment. Special-purposes entities may not get the same opportunities and exposure that established parent companies do. Some regulations may also apply to SPEs, which can cause problems for the parent companies. These may change regularly, which may have an adverse impact on the parent company's financial position. Similarly, some accounting standards may apply to these entities. Therefore, SPEs may not always stay off-balance sheets. ConclusionA special-purpose entity is a subsidiary company used to isolate financial risks or securitize assets. SPEs are useful when parent companies make risky investments or face bankruptcy. With these entities, parent companies can mitigate any risks they face. Special-purpose entities can have various advantages but may also come with some disadvantages. Article Source Here: What is a Special Purpose Entity Historical volatility (HV) is a useful measure to gauge market uncertainty. Recall that, In finance, volatility (usually denoted by σ) is the degree of variation of a trading price series over time, usually measured by the standard deviation of logarithmic returns. Historic volatility measures a time series of past market prices... Investors care about volatility for at least eight reasons:

Historical volatility is usually calculated by using the simple moving average of the historical returns. This approach works well when the market is in a “normal” condition. However, when there is a shock in the market, volatility increases and the equally weighted HV starts revealing its drawbacks, i.e.

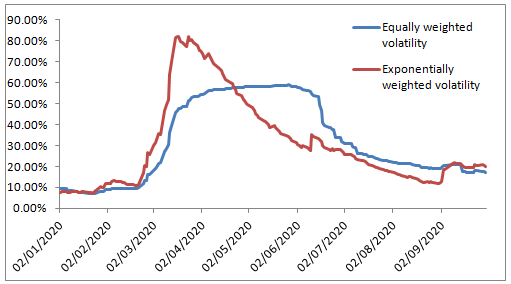

The picture below illustrates the above points. The blue line depicts the 3-month equally weighted historical volatility of SPY. As we can observe from the figure, when the SP500 went down in early March of 2020, the implied volatility (not shown) went up, but the equally weighted volatility was lagging. It started going up only a week later. By mid-June, the market started stabilizing, but the equally weighted historical volatility still exhibited a high value. And finally, the equally weighted HV dropped abruptly at the beginning of July.

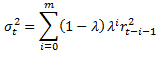

To remedy these problems, one can use the Exponential Weighted (EW) historical volatility that assigns bigger weights to the recent returns, and smaller weights to the past ones. The EW return variance is calculated as follows,

where λ is a weighting factor, σt denotes volatility at time t, m is the sample size, and rt denotes the daily return at time t. It is observed from the figure above that the EWHV (red line) is more responsive than the equally weighted historical volatility. Also, the decline of the EWHV from its peak is smoother than that of the equally weighted HV. The equally and exponentially weighted historical volatilities were implemented in an Excel workbook. Click on the link below to download the Excel workbook. Post Source Here: Exponentially Weighted Historical Volatility in Excel-Volatility Analysis in Excel What is Goodwill?Goodwill is a concept that is often prevalent in accounting. It is an intangible asset that companies acquire when they purchase another company. Usually, goodwill represents the difference between the purchase price and the net fair value of a company's net assets. When the sum that companies pay is higher than the net fair value of the net assets they get, the difference is considered goodwill. Usually, goodwill comprises various underlying assets. These include a company's brand name, customer relations, proprietary technology, customer base, etc. During a company acquisition, the parent company may be willing to acquire the company more than it is worth. In accounting, this premium that companies pay for acquisitions is considered goodwill. Is Goodwill an Asset?As mentioned, goodwill is the premium that companies pay for acquisitions. Therefore, goodwill is an asset that companies recognize in their Balance Sheets. Since it is an intangible asset that companies use for a long time, goodwill is a part of a company’s non-current assets. However, companies can only recognize it in specific conditions. Accounting standards require companies to recognize goodwill when they acquire another company. Since it is an intangible asset, all the provisions applicable to other intangible assets also apply to goodwill. Therefore, companies must have a valid basis to calculate its value. Like other intangible assets, companies cannot recognize internally-generated goodwill. It may be due to various reasons. Most importantly, it is because they cannot measure the value reliably. When companies purchase other companies, it provides a basis for goodwill calculation. Therefore, the recognition of goodwill is only possible when there is an acquisition. How to calculate Goodwill?Goodwill calculation is only relevant when one company acquires another company. As mentioned, they cannot calculate their internal goodwill for various reasons. Companies can use the following formula to calculate the value. Goodwill = Purchase price of the acquired company - Net fair value of the acquired company’s net assets The net fair value of the acquired company’s net assets is the residual amount after deducting its liabilities from its assets. As long as the above formula returns a positive result, the residual amount will be the goodwill. If it provides nil or a positive amount, it is not considered goodwill. In that case, companies cannot recognize it as an asset. Once companies calculate the goodwill for an acquisition, they can use the accounting treatment give below.

ExampleA company, Red Co., acquires another company, Blue Co., for $100 million. The net fair value of Blue Co.'s total assets on its Balance Sheet was $90 million and its total liabilities were $20 million. With this transaction, Red Co. paid for the acquisition more than Blue Co.'s worth. Therefore, the premium paid will be its goodwill. The calculation for goodwill for Red Co. will be as follows. Goodwill = Purchase price of the acquired company - Net fair value of the acquired company’s net assets Goodwill = $100 million - ($90 million - $20 million) Goodwill = $30 million Red Co. can recognize the amount in its accounts using the following double entry.

ConclusionGoodwill represents the premium that companies pay when purchasing another company. It represents the difference between the acquisition price and the net fair value of the acquired company's net assets. Goodwill is an intangible asset that companies must present on their Balance Sheet. Originally Published Here: Is Goodwill an Asset? Assets are a crucial part of any company or business. These are financial resources that companies own or control and can result in future economic inflows. In accounting, companies cannot charge an asset’s total costs to a specific period. Instead, they must distribute the cost using depreciation. However, assets may also suffer due to impairment. What is Impairment?Impairment is a term that is crucial in accounting and often associated with assets. It describes a permanent reduction in an asset's value. Impairment applies to all types of assets that companies own. The only exception is assets that have specific rules for impairment, for example, inventory. Impairment may come due to several external and internal factors. Essentially, impairment represents the difference between an asset's book value and its recoverable amount. The recoverable amount usually refers to any asset's fair value after deducting any selling costs. In some circumstances, it may also refer to an asset's value in use. When both are available, the recoverable amount is the higher of both amounts. How to calculate Impairment Loss?As mentioned, impairment loss represents the difference between an asset’s carrying value and recoverable amount. Therefore, the calculation of impairment loss requires companies to calculate their asset’s carrying value first. Usually, it is available in their Balance Sheet under the respective balance. Once companies determine the carrying value, they must establish a recoverable amount. Determining a recoverable amount may require some calculations. However, once they conclude the asset's recoverable amount, they must compare it with its carrying value. If the carrying value is lower than the asset’s recoverable amount, then there is an impairment loss. Companies can use the following formula to calculate the impairment loss. Impairment Loss = Asset’s Recoverable Amount - Asset’s Carrying Value In the above formula, the asset’s recoverable amount will be as follows. Asset’s Recoverable Amount = Higher of Asset’s Fair Value Less Cost to Sell or Value in Use If the impairment loss formula above returns a negative amount, the company must record an impairment loss on its income statement. If it is positive, then there is no accounting treatment for it. How do companies present Impairment Loss on Income Statement?An impairment loss is a non-cash expense for companies. Therefore, they must record it accordingly. Similarly, they must report the impairment loss on the Income Statement. The double entry to record impairment loss is as follows.

The impairment loss part of the double-entry will get reported on the Income Statement. The classification may depend on the company's preferences. Usually, however, companies may present it as an administrative or production expense. The other side of the entry will impact the company's Balance Sheet, reducing the asset's value. ExampleA company, Red Co., has an asset with a carrying value of $100,000. The asset’s recoverable amount in the market is $80,000. Therefore, there is an impairment loss of $20,000 ($80,000 - $100,000) on it. Red Co. must report the impairment loss on its Income Statement. Therefore, the treatment will be as follows.

ConclusionImpairment loss represents the negative difference between an asset's recoverable amount and carrying value. It is a crucial concept in accounting that companies must follow for almost every asset. An impairment loss is an Income Statement item as it represents an expense for companies. It also results in a decrease in the asset’s value in the Balance Sheet. Originally Published Here: Impairment Loss on Income Statement What is a Financial Contagion?A financial contagion represents the spread of a financial crisis from one entity or market to another. Financial contagions can occur within a single economy or can go beyond international borders. These usually include issues with currency exchange rates, stock prices, capital flows, etc. Financial contagions represent a potential risk for companies that want to integrate with international financial markets. Usually, the cause behind economic crises spreading in a region or between various countries comes to financial contagions. There are several factors that may play a role in it. For example, a country's financial systems failing can develop a financial contagion in the area. The failures can start as a domestic problem and spread to an international level. At a domestic level, financial contagions start with system failures. For example, a bank's inability to repay its customers can cause a contagion. It can spread to an international level and cause neighbouring countries to suffer as well. From there, it keeps transmitting to other economies as well, whether directly or indirectly related to these economies. How do Financial Contagions work?Contagions usually start with the transmission of economic crises. It may happen with a market or a region. Contagions are often adverse in their nature and can impact domestic and global economies. The reason for financial contagions becoming so prevalent is the globalization of various economies. More countries are dependent on each other in their economics, which makes financial contagions possible. Usually, financial contagions come in the form of crises or recessions. These can have a significant impact on related economies. It stems from one location and transmits to others, causing a widespread effect. It is also where financial contagions get is names from as they have the potential to spread quickly. Similarly, its unpredictable nature is one of the reasons why they are difficult to control. There are various reasons why financial contagions may start. In domestic markets, it may come due to a loss of trust in financial institutions. In international markets, it may come due to the globalization or interrelatedness of various economies. For example, countries that make global investments or indulge in cross-border trades may cause financial contagions. Usually, financial contagions have more impact on smaller economies, such as developing countries. These economies may not have the resources to absorb the impact of such widespread crises. However, for larger economies, financial contagions may not cause similar problems. These economies have the financial backing to support themselves. How can Financial Contagions impact economies?Financial contagions can cause damages to economies and financial systems. They can come in various sizes and forms, which makes it difficult to identify them. Financial contagions result in macroeconomic upsets on a local and international scale. The most critical impact for these is that they can spread, resulting in more damages than initially anticipated. There are several reasons why financial contagions can occur. For example, they may occur due to competitive currency devaluation or financial crises. According to economists, there are four agents that can contribute to it. These include governments, financial institutions, investors, and borrowers. ConclusionFinancial contagion is a concept that represents the spread of a financial crisis from a market to another. Financial contagions can cause widespread damage. Initially, they may start at a domestic level but may move to an international level eventually. Post Source Here: What is a Financial Contagion? There are many types of risks that are relevant to finance and the economy. Among these, systemic and systematic risk may be prevalent. However, due to similar names, most people confuse their meaning. However, both of them are different from each other. Therefore, it is crucial to understand them and how they differ from each other. What is Systemic Risk?Systemic risk represents the risk of a major failure of a company's financial system. It is the risk that relates to the collapse of an entity. These may include companies, industries, financial institutions, markets, or even economies. Systemic risk comes when capital providers lose trust in the users of their capital in a transaction. Systemic risk can cause widespread problems and can spread from one entity to another. Whether it is on a small scale or a large one, controlling or mitigating systemic risk is substantially challenging. Usually, governments need to intervene to restrain the spread of systemic risk to a larger level. However, sometimes it may be too late for a government to intervene. Systemic risks usually occur within larger organizations, such as financial institutions. These start with a single entity and have a cascading effect on others as well. Once stakeholders realize it, their subsequent actions can diffuse the risk to the market. This way, the systemic risk spreads to many market participants, eventually causing significant problems. What is Systematic Risk?Systematic risk is a type of risk that investors usually come across while investing. It is the opposite of unsystematic risk. Systematic risk refers to the risk associated with markets or market segments. This type of risk affects the overall market, unlike unsystematic risk, which impacts a particular company or industry. Other names used for systematic risk include market or undiversifiable risk. Like systemic risk, systematic risk can also apply to a large number of market participants. However, it does not spread outside the specific market. The systematic risk may come due to several types of risks, such as interest rate risks, inflation, industry risk, etc. For investors, systematic risk is unavoidable. As the name suggests, they can't diversify their investment portfolio against it. However, there are some methods that investors can mitigate the risk. For example, they can use asset allocation to spread their investment over several asset classes. This way, they don't bear the full effect of the market risk in case of any potential circumstances. Systematic risk is quantifiable, unlike other types of risk, such as systemic and unsystematic risks. Investors can significantly increase their exposure to systematic risk when they include only investments from a particular market in their portfolio. Any changes in the market, such as interest rates or inflation, can significantly impact their profitability. For example, any changes in the real estate market can impact shareholders that hold real estate property. Similar to systemic risk, systematic risk is highly unpredictable. ConclusionSystemic and systematic risks are two highly impactful risks. Due to their similar names, people often tend to mix them. However, they are different. Systemic risk is the risk of a major failure within an entity's financial system. It creates a cascading effect and can spread to other entities as well. Systematic risk is the risk that investors face with their investments in a particular market. It is a risk that impacts all investments in a specific market. Post Source Here: Systemic Risk vs Systematic Risk Capital refers to the financial assets that a company or business owns. For companies, having capital is crucial in daily operations. Mostly, it comes in the form of funds and physical assets that companies use. Sometimes, however, it may also come in the form of a company's workforce as human capital. There are many differences between physical and human capital. It is crucial to understand what these are and how they differ from each other. What is Human Capital?Human capital refers to the economic value of the workforce that works for a company. It may include things such as workers' experience, skills, education, training, etc. However, like physical assets, human capital is not tangible. While a company's workforce has a physical existence, their skills and experience are intangible assets, which is what companies value. Unlike physical capital, companies cannot recognize human capital in their financial statements. There are several reasons for that. Primarily, it is because the workforce isn't an asset that companies own or control. On top of that, it is not possible for companies to measure the value of human capital. Therefore, they cannot recognize it on their Balance Sheets. Despite that, human capital can bring value to any company. Most companies thrive to improve the working conditions for their employees to improve their performance. Therefore, they invest in their human capital by training and educating them. Usually, human capital is associated with more productivity which can lead to higher profitability. What is Physical Capital?Physical capitals include all tangible assets that companies own. These may consist of property, plant, equipment, inventory, cash, etc. Physical capital only includes man-made items. Therefore, capital such as human capital and natural resources are not a part of it. Usually, companies acquire or obtain these as a part of their business transactions. Physical capital is crucial in running companies. Almost every business will have physical capital. Unlike human capital, the value of physical capital is measurable. Similarly, it represents resources that companies own or control. Therefore, they must recognize it in their Balance Sheets. The recognition criteria may differ according to a company's policies. Physical capital, like human capital, can add significant value to a company and its operations. Companies don't need to bear continuous improvement costs on some of the assets within physical capital. However, it may come with higher initial costs for companies. What are the differences between Human and Physical Capital?There are several differences between human and physical capital. These include the following. SourceHuman capital comes due to the workforce that a company has. On the other hand, physical capital comes from any assets produced by humans. TangibilityHuman capital is intangible as it represents the experience, skills, and other aspects of a workforce. Physical capital usually includes tangible assets. TransactionsHuman capital does not come as a result of a company's transactions. Neither can companies sell or buy it. However, physical capital comes from a company's transactions and can be sold and purchased. ReportingCompanies cannot report their human capital on their financial statements. However, physical assets are a part of companies’ Balance Sheets. ConclusionCompanies need both human and physical capital to operate. However, both of these are different. Human capital represents the experience, skills, talents, etc., of a company’s workforce. On the other hand, physical capital represents man-made assets. Article Source Here: Human Capital vs Physical Capital What is Gross Domestic Product?Gross Domestic Product (GDP) refers to the total value of all goods and services produced within a country. It confines these goods and services to a specific country's borders within a particular period. Usually, a country's GDP is an indicator of how well its economy is doing. Likewise, higher GDP means a country has a better economy. Calculating a country's GDP includes aggregating the value of all the finished goods or services in the country. For that purpose, any goods or services that go into those finished goods do not contribute to the total value. Similarly, the calculation considers several factors about a specific country's economy. These many include consumption and investments. What are the types of Gross Domestic Product?There are several types of GDP that economists may use to gauge a country's economic prowess. Therefore, it is crucial to understand what these are and how they differ from each other. These include the following. Nominal Gross Domestic ProductNominal GDP refers to the total value of all goods and services at current market prices. Another name used for this type of GDP is the “current-dollar” GDP. A country’s nominal GDP represents a raw measurement that includes price increases. Usually, it does not consider any inflation or deflation in the economy. Real Gross Domestic ProductReal GDP is the opposite of nominal GDP. It considers inflation and deflation in the economy. A country's real GPD refers to the sum of all goods and services produced at constant prices. The prices used in real GDP have a base year, which is usually the year before it. Real GPD provides an accurate measurement of economic growth over a period. Gross Domestic Product Growth RateGDP growth rate is a term used to compare how fast a country's economy grows from one period to another. It comes in the form of a percentage. Countries may have positive or negative GDP growth rates. The goal for every country is to have a positive growth rate. It is because negative GDP growth rates may be an indicator of possible recessions in the future. Gross Domestic Product Per CapitaAnother type of GDP most prevalently used by economists is GDP per capita. It is a measure of a country's GDP per person in its population. GDP per capita is a comparative tool that economists use to compare the GDP between several countries. GDP per capita may also come in different forms such as nominal and real GDP per capita. Why is Gross Domestic Product important?A country's GDP can represent its economic production and growth. It affects everyone living in that country in several ways. For investors, a country's GDP can be a factor when deciding foreign investments with asset allocation. With GDP, analysts can determine whether a country's economy is improving or moving towards a recession. GDP is also crucial for governments. Based on the GDP calculation, a country's government can decide on several policies. For example, it may include both fiscal and monetary policies related to the country. In turn, these decisions can impact any stakeholders who primarily reside within the country. Overall, a country's GDP can be significantly critical for all involved parties. ConclusionGross Domestic Product is a term used to represent the total value of finished goods and services produced in a country. There are several types of GDPs, including nominal and real GDP, GDP growth rate, and GDP per capita. A country's GDP can be crucial for governments, investors, and any other stakeholders. Originally Published Here: What Is Gross Domestic Product? |

Archives

April 2023

|

RSS Feed

RSS Feed