Derivative Valuation, Risk Management, Volatility Trading

|

Investors can use various active management strategies to manage their portfolios. Usually, they hire a portfolio manager to track the performance of their portfolio. The managers can make decisions regarding the portfolio with the goal of outperforming the market. However, they must also manage the risks associated with it. One strategy that is common in active management is Tactical Asset Allocation. What is Tactical Asset Allocation?Tactical Asset Allocation (TAA) is an active management portfolio strategy that focuses on three primary asset classes. These include stocks, bonds, and cash. The goal with TAA is to shift the percentage of assets held in these categories to benefit from market pricing anomalies. With this strategy, portfolio managers can create extra value by exploiting various market events or situations. Usually, managers determine a balanced mix of several asset categories. However, they may change this mix to benefit from anomalies. Once they have exploited the market situations, they can revert to their original asset mix. This way, they can ensure both diversification of portfolios and higher returns. How does Tactical Asset Allocation work?Investors can use the tactical asset allocation by themselves or hire a portfolio manager to take care of it. Usually, the portfolio manager determines a prudent mix of assets that suits the investors' risk tolerance. Similarly, the manager also considers the investment objectives for the portfolio when deciding on the asset mix. Managers divide the portfolio into three asset categories, which include stocks, bonds, and cash. They use the determined mix for the allocation. However, the mix does not remain constant. The manager will change the allocation depending on the prominent market and economic conditions. The allocation to a particular asset may vary according to these conditions and the investors' objectives. Therefore, it may be neutral-, over-, or under-weighted. Managers may include these factors as a part of the investment policy statement. For example, managers may use the following simple mix of assets in a typical portfolio allocation. The percentage for each asset class represents its weight. Stocks = 50% Bonds = 30% Cash = 20% The above is an example of the long-term mix that managers will follow to help investors reach their specific goals. However, they may change it when they can find any anomalies in the market. Once they exploit those conditions, they will return to the long-term mix. What is the importance of Tactical Asset Allocation?Tactical asset allocation can be beneficial for investors for several reasons. Firstly, it allows investors to increase their returns. By changing their asset mix within a portfolio to benefit from market conditions, investors can increase their returns. Similarly, it allows for adaption according to market conditions. Unlike passive management strategies, tactical asset allocation changes according to the market. Therefore, investors can benefit from any changes in the market and not suffer due to adverse fluctuations. Most importantly, tactical asset allocation promotes diversification. Investors can diversify their portfolios by allocating them to different asset categories. Similarly, TAA allows investors to choose their own asset mix, allowing for even better flexibility. ConclusionTactical asset allocation is an active management strategy. Investors use it to divide their portfolio into various asset categories. Once they identify any market anomalies that they can exploit, they can change the asset mix to generate higher returns. After that, they can revert to their original mix and wait for the next opportunity. Article Source Here: What Is Tactical Asset Allocation

0 Comments

Investors can use both the Treynor and the Sharpe ratio to measure the risk-adjusted rate of return. However, both are different from each other. While both can help investors gauge the risk on their investments, they both use a different approach to do so. Therefore, it is crucial to understand how both of these work for investors. What is the Treynor Ratio?The Treynor Ratio is a metric to determine how much excess return investors can generate for each unit of risk they take on their portfolio. The ratio calculates the return that investors earn above what they could get on a risk-free investment. For this purpose, investors can use the risk-free rate of return, usually taken as the rate on government treasury bills. The Treynor ratio takes the systematic risk of a portfolio in the form of beta. It produces a meaningful result if an investment’s beta is positive. Similarly, it measures a portfolio return’s tendency to change with fluctuations in the overall market. An alternative name used for the Treynor ratio is the reward-to-volatility ratio. The formula for Treynor Ratio is as below. Treynor Ratio = (Portfolio return - Risk-free rate of return) / Beta of the portfolio The purpose of investors with this ratio is to measure how successful an investment is in compensating them for taking investment risk. It depends on a portfolio's beta to judge risk. Investors always want to take risks only if they can receive compensation in the form of higher returns. However, these are risks inherent to the portfolio, which they cannot mitigate through diversification. What is the Sharpe Ratio?The Sharpe Ratio helps investors determine the return of an investment compared to its risk. It takes the average return that investors earn more than the risk-free rate per unit of volatility or total risk. Volatility is a measure of the price fluctuations of an investment or portfolio. The Sharpe Ratio also considers the rate on government treasury bills as the risk-free rate. Through the Sharpe Ratio, investors can determine whether they are getting excess returns due to their investment decisions or taking up more risk. Investors can use the ratio to evaluate a portfolio’s past and expected performance. Unlike the Treynor Ratio, the Sharpe Ratio considers the diversifiable risks of a portfolio. The formula to calculate the Sharpe Ratio of a portfolio is as below. Sharpe Ratio = (Return on portfolio - Risk-free rate of return) / Standard deviation of the portfolio’s excess return The Sharpe Ratio focuses on maximizing returns and reducing volatility for investors. Usually, a higher Sharpe Ratio is preferable for investors. It is because it indicates a higher investment return relative to the amount of risk that investors take. What are the differences between Treynor and Sharpe Ratios?The difference between both the ratios comes down to the risks they consider. The Treynor Ratio takes the systematic risk of a portfolio, the beta, to measure volatility. On the other hand, the Sharpe Ratio considers the portfolio's standard deviation to do so. Both ratios also have different meanings. The Treynor determines the excess return generated for each unit of risk in a portfolio. In contrast, the Sharpe Ratio helps investors understand their investment’s return compared to its risk. ConclusionInvestors can use two ratios to measure the risk-adjusted rate of return for their portfolios. These include the Treynor and Sharpe Ratios. The Treynor Ratio looks at the excess return that investors can get for each unit of risk they take on their portfolios. The Sharpe Ratio measures the return on investment compared to its risk. Originally Published Here: Treynor Ratio vs Sharpe Ratio Investors use various investment strategies to ensure they maximize their returns. Some of these strategies may be long-term, while others may last for a short time. Each type of strategy has its own benefits and drawbacks. One strategy often used by investors and speculators is short selling. What is Short Selling of Stocks?Short selling is an investment strategy in which investors speculate about the decline in a stock's price. Based on these speculations, they buy or sell stocks in the market. Short selling is a risky strategy because it has the potential to result in high losses. Therefore, it is crucial that only experienced investors with knowledge of the market use this strategy. Short selling involves selling stock that sellers don't own or that they have obtained through a loan from a broker. Short sellers use this technique because they may speculate a stock's price will go down. They believe that if they sell the stock now, they can buy that stock later for a lower price. By doing so, they make a profit from the difference between the buy and sell prices. What are the risks associated with Short Selling?As mentioned, short selling involves significant risks, especially for investors without any market knowledge. When investors buy a stock, they take a risk with the amount they pay to purchase it. The maximum amount that the investor risks is the value paid for the purchased stock. However, with short selling, the risk is not limited to that price. Investors can make losses more significant than the price they pay for a stock. In theory, they can lose an infinite amount of money. Investors can continuously make losses because the stock may continue to go up in value indefinitely. In some cases, investors may end up in a net liability position and owe money to the brokerage. What are the advantages and disadvantages of Short Selling?There are various pros and cons of short selling. Investors can benefit if they make the right speculations. Usually, they don't need a large initial capital as most of the strategy involves borrowing from brokers. It is also possible to make leveraged investments through short selling. Through the right short selling strategy, investors can hedge against other holdings, providing a balance to their overall portfolio. However, short selling can also potentially result in unlimited losses for the investor. It is also a strategy that only experienced investors can use beneficially. For newer investors, short selling can be substantially risky. Short selling also requires a margin account. This strategy also comes with margin interest, which can be a significant expense when margin trading. When should investors use a Short Selling strategy?Short selling works when stocks go down in value. Often, however, the expectation is that stocks go up in value. In these circumstances, therefore, a short-selling strategy is not beneficial. Similarly, buying stocks is less risky compared to short selling. When investors can predict a downfall in stock prices, short selling can prove to be highly beneficial. ConclusionShort selling is a strategy that investors use to speculate the downfall in the prices of shares. When investors predict a drop in stock prices, they sell their stocks to purchase them back later at a reduced price. This way, they can profit from the difference in prices. Short selling is a risky strategy. Investors need to have some prior market and investing experience to make the strategy work. Originally Published Here: Short Selling of Stocks Risk defines a degree of uncertainty that may come during various stages in an entity's lifecycle. The concept of risk is most prevalent in economics and finance. For businesses or investors, identifying and dealing with risk is crucial. It also helps to understand the differences between the types of risk to understand how to mitigate them. For investors, the difference between systematic and unsystematic risk is critical to define. These are risks that accompany every financial decision. Therefore, it is crucial to know the differences between both of them. What is Systematic Risk?Systematic risk represents the risks that are inherent to the entire market or market segment. It affects all market participants similarly and not just a specific stock or company. Other names for systematic risks are undiversifiable, volatility, or market risk. Systematic risks come from various sources and are unpredictable and inevitable. Investors can use various strategies to mitigate other types of risks, such as diversification. However, most of these strategies do not work for systematic risk. It is because this risk affects the overall market. However, there are still ways to mitigate these risks. Investors can use strategies, such as asset allocation or hedging, to manage systematic risks. What is Unsystematic Risk?Unsystematic risk represents risks that relate to a specific company or industry. This risk is inherent to a particular stock, company, or industry rather than the market as a whole. Other names for unsystematic risk include specific, diversifiable, or residual risk. The unsystematic risk may come from external factors, such as new competitors, or internal factors, such as bad performances. The most common strategy that investors use to mitigate unsystematic risk is diversification. As unsystematic risks relate to specific investments, investors can construct a diversified portfolio to manage them. Investors can sometimes use various techniques to anticipate or predict unsystematic risks. However, it is not always possible to predict it. What are the differences between Systematic and Unsystematic Risk?There are many differences between systematic and unsystematic risk. A few of those differences are as below. DefinitionSystematic risks represent risks that apply to the market as a whole. Unsystematic risks, on the other hand, are risks that are specific to a company or industry. NatureSystematic risks are uncontrollable and unpredictable in their nature. Therefore, traditional diversification strategies may not work with systematic risks. However, unsystematic risks are usually controllable and diversifiable. MeasurementThe best measurement of systematic risk is the Beta coefficient. Unsystematic risk, in contrast, does not have a measurement unit. However, investors can calculate these risks by deducting the systematic risk from the total risk. SourcesSystematic risks come from external sources. These include risks such as interest rate risks, material risks, purchasing power risks, etc. Unsystematic risks may come from internal and external sources. These may consist of financial, business, and operational risks, among others. MitigationAs mentioned, the best way to mitigate systematic risk is through asset allocation. However, for unsystematic risk, investors can use diversification to mitigate them. ConclusionSystematic and unsystematic risks are critical in finance and investing. Systematic risks represent these risks that apply to the market as a whole. On the other hand, unsystematic risks apply to a specific stock or industry. There are various other differences between both these risks, as mentioned above. Article Source Here: Systematic Risk and Unsystematic Risk There are two terms related to the risk that are crucial for investors to understand. These are risk tolerance and risk appetite. Both of them have various similarities. However, there are also some differences between them. What is Risk Tolerance?Risk tolerance represents the amount of risk that investors can tolerate when building their investment portfolio. Risk tolerance shows the degree of uncertainty or variability in investment returns that investors can withstand before exiting the market. Usually, an investor’s risk tolerance level depends on various factors, including their financial situation, time horizon, purpose, preferences, etc. The most critical factor among those is the investor’s age. Usually, younger investors have a higher risk tolerance level compared to elders. It ties various of the above factors together. For example, younger investors have a longer time horizon. Therefore, their purpose is to make higher returns. Hence, they are also likely to accept higher risks associated with their investments. There are various categorizations for investors based on their risk tolerance. For example, some investors may not tolerate higher risk. These investors may take a cautious approach to investments. Therefore, they will have conservative risk tolerance. On the other hand, investors with a preference for higher returns and risk will have aggressive risk tolerance. Lastly, those with a balanced approach will have moderate risk tolerance. What is Risk Appetite?Risk appetite represents the amount, percentage, or rate of risk that an investor is willing to accept. Risk appetite is the quantification of an entity's willingness to take risks in return for its plan, objectives, and innovation. Risk appetite is closely related to risk tolerance levels. However, it does not represent the level of risk before an entity leaves the market. Instead, it refers to the risk they are willing to accept when executing their plans or strategies. Most investors or businesses have a risk appetite framework. This framework helps the consciously recognize the risks and acknowledge the potential exposure to their strategies. This framework depends on how entities view the relationship between risks and rewards for their chosen plans or strategies. While risk appetite usually relates to an entity, it may also get affected by regulatory or legal requirements. Entities with a higher risk appetite are also willing to accept higher uncertainty and volatility in exchange for higher growths. On the other hand, entities with a lower risk appetite will have a risk-averse approach to their plans and strategies. They will prioritize stability and lower growth over market volatility and higher returns. What is the difference between Risk Tolerance and Risk Appetite?The difference between both risk-related concepts is subtle. Risk tolerance is when entities would remain comfortable despite losses or uncertainties. Their risk endurance depends on several factors such as age, earning capacity, time horizon, etc. Every investor will have their own personal risk tolerance levels. Risk appetite represents the amount, rate, or percentage of risk that entities are willing to bear in their planning or strategy. It comes as a direct result of an entity’s goals or objectives. These are risks that entities must accept to move forward with their chosen path. ConclusionRisk tolerance and risk appetite are terms associated with risk that have similar meanings. Risk tolerance refers to the level of risk that entities are willing to accept when constructing a portfolio. On the other hand, risk appetite is the risk they must take in their plans or strategies. Article Source Here: Risk Tolerance vs Risk Appetite What is Risk Aversion in economics?Risk aversion is a term often associated with economics and finance. It describes the tendency of people to prefer low uncertainty outcomes to those with high uncertainty. Risk aversion applies to several other fields of life as well, such as investing. Risk-averse people are likely to reject higher risks even if they can get higher returns from accepting these risks. Risk aversion explains why people prefer to agree to a situation that is more predictable with lower returns. Risk-averse investors will always choose to get low predictable returns or outcomes rather than high unpredictable ones. For example, these investors may prefer putting their money in the bank and earning steady investing returns. They don't consider any alternatives when the outcome is not predictable. Why is Risk Aversion essential?Risk aversion is a crucial concept in economics and for investors. Investors that are significantly risk-averse prefer investments that offer guaranteed outcomes. For these investors, investing in risk-free instruments or those with similar risk levels is the best option. Risk aversion explains why investors may not always prefer high returns, as they come with high risks. For example, risk-averse investors prefer investing in government treasury bonds and certificate of deposits. On the other hand, risk-loving investors may go with aggressive investing strategies to obtain higher returns. Among both these extremes, there are also risk-neutral investors that prefer moderate risks with moderate returns. What are the characteristics of Risk-Averse investors?Risk-averse investors or individuals have various characteristics. Usually, they have a conservative approach to selecting investments or projects. They don't prefer to include any volatile investments in the portfolio. Usually, risk-averse investors prefer highly liquid assets. The demand for liquidity comes due to their preference for financial security over performance. Several factors can play a role in making someone risk-averse or risk-seeking. Usually, the investor's age is the most critical factor. It is common for older investors to be more risk-averse, as they prefer steady incomes for financial stability. Younger investors, on the other hand, are more risk-seeking on average. However, other factors, such as the investor's background, financial history, and experiences may also dictate their risk level preferences. What are some investment choices for Risk-Averse investors?Some investment choices are prevalent among risk-averse investors. The reason for the high demand is that they come with high levels of certainty for investors. Among the most common investment choices for risk-averse investors are the following.

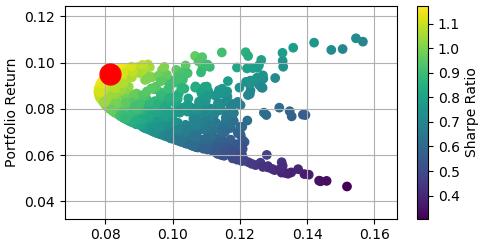

Almost all of the above investment choices come with high levels of predictability and certainty. Some, like dividend growth stocks, may fluctuate in value. However, these are usually stocks of stable, well-established companies. Therefore, the fluctuations aren’t as substantial compared to other companies. Similarly, the steady source of growing income from dividends is a highly favourable option for risk-averse investors. ConclusionRisk aversion is a concept usually associated with economics and finance. In the world of finance, it has significant importance as well. Risk aversion describes why people tend to prefer low returns if they come with higher certainty. It also explains why some investors may be risk-averse, while others may be risk-seeking or risk-neutral. Article Source Here: Risk Aversion in Economics and Finance When companies or businesses come across risks, they use various risk management techniques. For every type of risk that a company identifies, it must assess its probability, importance, and frequency. Based on that, it must evaluate what strategy to use to manage it. Among the various risk management techniques, companies may use risk transfer to mitigate risks. What is Risk Transfer?Risk transfer refers to the risk management technique in which companies transfer their risk to a third party. Usually, the third party will charge these companies to accept it. A risk transfer happens when one party assumes the liabilities of another party. It is often prevalent in insurance transactions, where companies transfer their risk to an insurance agency or company. However, risk insurance may also happen between various other parties. For example, individuals may transfer their risks to other individuals. Or individuals may transfer their risks to insurance companies. However, the process does not end there. Some insurance companies even further transfer their risks to reinsurers. The chain created by risk transfer may involve several parties at the same time. How does Risk Transfer work?As mentioned, risk transfer is most prevalent within insurance transactions. It is the best way to describe how risk transfer works. Firstly, a company or an individual identifies a risk that they want to mitigate through transferring. The risk may come with potential losses or adverse outcomes. Therefore, they may want to shift those losses to a third party. Once a company decides to transfer risks, it must find a third party willing to accept it. Through risk transfer, companies can't eliminate the risk. However, they shift it to another party. Therefore, the risk always exists, and one party must suffer the consequences arising from them. However, the opposite party may also benefit from the transaction by charging a fee for accepting the risk. What are the ways in which companies use Risk Transfer?There are two ways in which companies may transfer their risks. These are as below. Insurance contractsPurchasing insurance policies is one of the most prevalent risk transfer techniques that companies use. When an entity purchases insurance, they are shifting their financial risks to an insurance company. In exchange for the fee, the insurance company charges the entity a fee. In the case of insurance contracts, it is an insurance premium. Indemnification clauseCompanies may also include an indemnification clause in their contracts. It is a clause that ensures that any potential losses in an agreement will be the opposite party's responsibility. In short, companies include this clause in their contracts so that they get compensated for any losses. What is Risk Transfer in the insurance industry?As mentioned, insurance companies may also transfer their risks to a third party. The third-party, in this case, is known as a reinsurance company. These are companies that provide insurance to insurance companies. Similar to regular insurance transactions, insurance companies can also shift their risk to a reinsurance company. In exchange, the reinsurance company charges the insurance company an insurance premium. ConclusionRisk transfer is a risk management technique utilized by companies to mitigate any risks. The most common example of risk transfer is insurance contracts. However, companies may also use indemnification clauses in their contracts for similar purposes. Originally Published Here: Risk Transfer in Insurance For companies and businesses, identifying and managing various types of risks are crucial. Mostly, companies use traditional financial risk management techniques to mitigate them. Due to their nature, financial risks are most prevalent for companies. Therefore, these companies often focus on financial risks compared to other types. What are Non-Financial Risks?Apart from financial risks, companies may also come across non-financial risks. These are risks that are not a part of the standard financial risks of a business. Therefore, traditional risk management techniques don't cover them. Despite that, companies must identify and mitigate these risks. While these risks may not be as prevalent, they can still harm a company and its business. In its lifetime, a company will come across various types of non-financial risks. Identifying each of these non-financial risks allows the company to customize its responses accordingly. Most non-financial risks come from outside the company or due to external factors. However, there are still ways to mitigate these risks once a company identifies them. What are the types of Non-Financial Risks?Non-financial risks can come from various sources and can have different consequences. Given below are some of the most prevalent non-financial risks that companies often face. Reputational RiskReputational risk is a risk that can threaten or endanger a company's goodwill. For most companies, developing a brand name or goodwill with customers is crucial to long-term success. However, some factors may impact them adversely. These factors result in reputational risk for the company. These risks can come from within or outside the company. Reputational risks may come directly from a company's actions. These can stem from the decisions a company makes. Similarly, it may also come indirectly through an employee’s actions. Lastly, reputational risks may also generate tangentially through related or peripheral parties, such as suppliers, customers, or joint venture partners. Legal RiskLegal risk represents the risk that legal issues may impact a company's operations or reputation. For companies, legal risks may come directly as a consequence of their actions. For example, if a company sells faulty equipment to a customer that causes damage, it faces legal action. However, legal problems may also arise from external factors. Legal risks may also come in the form of regulatory risk. Companies abide by various rules and regulations. However, there's always that non-compliance with any of those regulations can impact their reputation or business. Regulatory risks can result in penalties and can give rise to financial risks and business risks. Model RiskModel risk represents the type of risk that a company's financial model fails. Usually, companies use their financial model to measure quantitative information, including value transactions or market risks. Companies rely on the results produced from these models for various purposes, including decision-making. Financial models have become prevalent in most companies. These models come with several calculation techniques or assumptions, which can be risky. Based on the information obtained from these models, companies make various estimates or forecasts. A small error in these models can lead to huge errors later when companies extrapolate the data. ConclusionDespite most companies focusing on financial risks, non-financial risks may also impact a company. Non-financial risks are risks that are not part of a company's traditional risk management techniques. There are various types of non-financial risks. Among these, companies most often face reputational, legal, and model risks. Article Source Here: Types of Non-Financial Risks Companies or businesses face various types of risks during their lifetime. Identifying and dealing with these risks is crucial for the long-term survival of those companies. While there are some risks that may not occur often, there are some others that companies must manage continuously. Among these, financial risks are prevalent. What are Financial Risks?Financial risks represent the possibility of losing money on investments or projects taken up by companies. These come from uncertainties related to the decision-making regarding investments. They can result in the loss of capital for companies and their stakeholders. However, companies aren’t the only entities that must face financial risks. Public entities, such as government bodies may also have to deal with financial risks. For these entities, financial risks represent the uncertainties related to the control of their monetary policies. Similarly, it may come as a result of a default on bonds or other debt issues. For government entities, financial risks come as a direct result of their finances or investments. For companies, on the other hand, financial risks may come from various sources. For example, failures within a company’s operations can result in the loss of profits and lead to capital losses. Similarly, financial risks can come from within or outside the company. There are various types of financial risks in business that companies must identify and mitigate. What are the types of Financial Risks in business?As mentioned, financial risks may come in various sizes and shapes. While there are several types of these risks, some of the most prevalent ones are as below. Market RiskMarket risk is the risk of changing conditions in a marketplace in which a company operates. Another name for market risk commonly used in investing is systematic risk. Various types of market risks can affect a company's performance. These may include interest rate risks, commodity risk, or currency risk. For each type of market risk, companies must have proper responses. Since the risk depends on a specific company’s situations and processes, market risk can differ between companies. Credit RiskCredit risk comes as a direct consequence of a company's credit system. When a company makes credit sales, it also undertakes credit risks. These risks come in the form of bad debts when customers fail to pay their owed money. Companies can also make credit purchases from suppliers. Therefore, credit risks also include risks related to those credits. Liquidity RiskLiquidity risk relates to the liquidity of assets or operational funding. This risk usually relates to the company's cash flows or working capital. Since these are vital aspects of a company's business, liquidity risk can prevent companies from making profits. For some companies, liquidity risk may be higher than others due to the nature of their operations. ConclusionFinancial risks consist of risks related to a company’s investments or projects. These can result in capital losses for a company. There are several types of financial risks in business. These include, but are not limited to, market, credit, and liquidity risks. Article Source Here: Financial Risks in Business Modern Portfolio Theory-Searching For the Optimal Portfolio-Portfolio Management in Python1/25/2021 In the previous installment, we presented a description of the Model Portfolio Theory and provided a concrete example in Python. We also explained the concept of an Efficient Frontier and provided a visual presentation of it. Recall that, ... the efficient frontier (or portfolio frontier) is an investment portfolio which occupies the "efficient" parts of the risk–return spectrum. Formally, it is the set of portfolios which satisfy the condition that no other portfolio exists with a higher expected return but with the same standard deviation of return (i.e., the risk). The efficient frontier was first formulated by Harry Markowitz in 1952. A combination of assets, i.e. a portfolio, is referred to as "efficient" if it has the best possible expected level of return for its level of risk (which is represented by the standard deviation of the portfolio's return). Here, every possible combination of risky assets can be plotted in risk–expected return space, and the collection of all such possible portfolios defines a region in this space. In the absence of the opportunity to hold a risk-free asset, this region is the opportunity set (the feasible set). The positively sloped (upward-sloped) top boundary of this region is a portion of a hyperbola and is called the "efficient frontier". Read more In this follow-up post, we are going to search for the optimal portfolio, i.e. one that has the highest risk-adjusted return. To do so, we will maximize the portfolio’s Sharpe ratio. The Sharpe Ratio is a financial metric that helps investors determine the return of an investment compared to its risk. It presents the average return that investors earn above the risk-free rate per unit of volatility or risk. The higher the Sharpe Ratio of a portfolio, the better it is in terms of risk-adjusted return. Our hypothetical portfolio consists of 3 Exchange Traded Funds: SPY, TLT, and GLD which track the S&P500, long-term Treasury bond, and gold respectively. We downloaded 10 years of data from Yahoo Finance and utilized a Python program to search for the optimal portfolio. The figure below shows the Efficient Frontier along with the optimal portfolio (depicted by the red dot).

The figure below shows the optimal portfolio’s composition, return, volatility, and the Sharpe ratio.

Click on the link below to download the Python program. Post Source Here: Modern Portfolio Theory-Searching For the Optimal Portfolio-Portfolio Management in Python |

Archives

April 2023

|

RSS Feed

RSS Feed